Saudi Infrastructure: Selective Capital, Continued Execution

Recent geopolitical tensions have inevitably raised questions around investor sentiment, supply chain resilience and the near term outlook for capital deployment across the Gulf. Yet within Saudi Arabia’s energy and infrastructure markets, the more important story is not whether activity pauses altogether, but how capital allocation becomes more selective.

The Kingdom’s infrastructure ambitions remain substantial, but today’s environment increasingly rewards strategic importance, resilient project fundamentals and alignment with long term national priorities.

The market backdrop has clearly become more complex. Elevated global inflation, higher for longer interest rates and regional geopolitical uncertainty have all contributed to a more disciplined financing environment. As a US dollar-pegged economy, Saudi Arabia inevitably imports much of the global monetary backdrop through its exchange rate framework, meaning tighter US monetary conditions continue to feed through into domestic funding costs.

However, that does not automatically translate into a broad slowdown in infrastructure execution. The more accurate interpretation is that capital is becoming more selective.

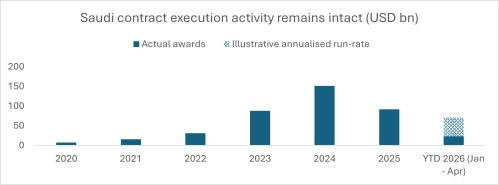

Project momentum remains intact

Strategic infrastructure transactions continue progressing despite a more uncertain backdrop. The additional financing for Prince Mohammad bin Abdulaziz International Airport in Madinah reaching financial close in March 2026, during the period of heightened regional geopolitical tension, is a tangible example that capital mobilisation into strategic infrastructure has not stalled.

The chart below provides a useful directional indicator, tracking Saudi project awards progressing into execution. While 2026 remains a partial year view, activity remains encouraging, particularly given the illustrative run-rate is based on the first four months of the year, which include the typically slower Ramadan and Eid period.

Importantly, this is not simply a story of legacy projects continuing through existing financing cycles. New strategic programmes continue to enter procurement, reinforcing confidence that momentum remains intact.

Saudi Arabia’s recently launched 3GW battery energy storage tender is a clear example, reflecting continued commitment to grid resilience and energy transition infrastructure. Likewise, the Ministry of Energy’s launch of natural gas distribution tenders across multiple industrial cities reinforces that critical enabling infrastructure remains a strategic priority.

This broader strategic focus also appears increasingly reflected in institutional capital allocation. Reuters recently reported that PIF intends to increase domestic deployment from approximately 70% to 80% of capital allocation under its latest strategy, reducing international weighting accordingly, a signal that strategic domestic infrastructure remains central to the Kingdom’s investment priorities.

Source: MEED Projects and Forvis Mazars analysis

Funding is available, but more selective

Saudi banking system liquidity has tightened incrementally over recent years, with private sector credit growth materially outpacing deposit growth. This reflects a more selective lending environment where banks must increasingly manage balance sheet capacity, pricing discipline and sector exposure more carefully.

Source: Saudi Central Bank (SAMA), monthly banking statistics

This dynamic is further reinforced by SAMA’s implementation of the Countercyclical Capital Buffer (CCyB), which became effective on 25 May 2026 and adds another layer of prudence around capital deployment.

Against this backdrop, lenders are naturally becoming more selective in how capital is allocated. Yet strategic infrastructure, particularly projects supported by strong counterparties, robust contractual frameworks and sovereign alignment, continues to retain strong credit appeal.

Importantly, the broader funding ecosystem also continues to deepen. Saudi Arabia’s local currency debt market is set to gain greater international relevance through the inclusion of SAR denominated government sukuk in both JPMorgan’s Government Bond Index – Emerging Markets (GBI-EM) and Bloomberg’s Emerging Market Local Currency Government Index. While this is not a direct project finance funding dynamic, it reflects the continued maturation and institutionalization of Saudi Arabia’s capital markets, supporting broader long term financing depth and flexibility.

Saudi financing markets continue to operate in a significantly higher rate environment than the ultra low cost conditions seen in prior years. While benchmark rates have moderated from peak levels, funding costs remain elevated relative to historical norms. For sponsors, this directly affects debt pricing, project returns, refinancing assumptions and capital structuring discipline.

Source: Saudi Central Bank (SAMA), 3M SAIBOR

Beyond benchmark rates, the question naturally turns to debt margins. Based on recent market discussions and strategic infrastructure transactions we have observed, there is no clear evidence to suggest material margin dislocation arising directly from recent regional geopolitical tensions. Where margin repricing has occurred, this appears to have been more closely linked to broader domestic liquidity tightening rather than the immediate geopolitical backdrop.

That said, the impact is unlikely to be uniform across all projects. Current lender caution appears less focused on pure lending margins and more on execution risk. Supply chain resilience, insurance coverage, EPC pricing pressure and broader delivery risk are all receiving heightened scrutiny, particularly for larger or more complex transactions.

For sponsors, this distinction matters. Even where lending margins remain relatively stable, higher project costs and more conservative lender assumptions, including the potential requirement for larger contingency buffers, can place pressure on project economics, increase equity requirements and ultimately reduce debt capacity. In that sense, the more immediate challenge may not be wider debt margins, but whether projects can continue to support the same financing structures in a higher cost execution environment.

I regularly share views and observations on developments across the energy and infrastructure markets. The perspectives expressed in this article are my own and do not necessarily reflect those of my firm.

Want to know more?