Vision 2030 Is Entering Its Execution Phase: What the Capital Numbers Are Telling Us

Editor’s note: This article was written prior to the recent geopolitical conflict in the region. It is still too early to fully assess the impact, and much will depend on its duration. What is clear, however, is that energy and infrastructure remain central to economic stability and strategic priorities across KSA. In the near term, private capital may become more selective or slow deployment (despite continued financial close activity), while sovereign and state linked capital plays a more prominent role in sustaining momentum. As visibility improves and risks are better understood, private capital is likely to re-engage at pace.

For much of the past decade, Vision 2030 has been framed in terms of ambition, reform agendas, diversification targets, and institutional redesign. What now matters more is not what is being announced, but what is being financed and delivered.

The capital data suggests a structural shift: Saudi Arabia has moved from policy signalling to measurable execution.

That distinction matters. Execution is the point at which strategy becomes investable.

Capital deployment has scaled materially

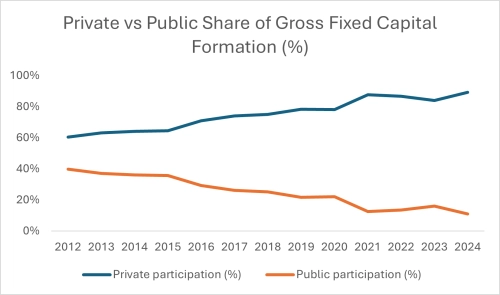

Gross fixed capital formation (GFCF) has accelerated sharply in recent years, rising from roughly $180–200bn annually through the mid-2010s to approximately $350bn in 2024.

This reflects a broad based expansion in infrastructure, energy, industrial capacity, and development activity.

Importantly, the composition of that capital has shifted. Private participation in GFCF has steadily increased over the past decade, now representing close to 90% of total capital formation.

This is not simply a matter of volume, it is a structural transition toward market led deployment.

In early development phases, capital is often state anchored and policy driven. As markets mature, private balance sheets increasingly take the lead. The data suggests Saudi Arabia is firmly in that latter phase.

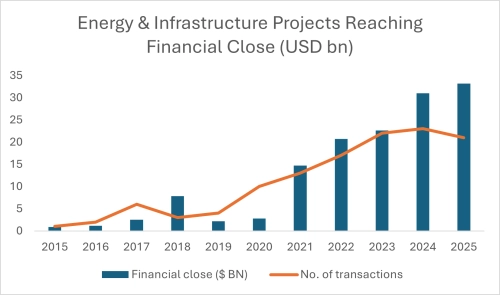

Financial close activity confirms execution depth

Capital formation tells us money is being deployed. Financial close data tells us projects are bankable.

Energy and infrastructure projects reaching financial close in Saudi Arabia have expanded materially over the past several years, rising from low single digit billions annually in the mid-2010s to over $30bn in recent years. This is a meaningful shift.

Financial close represents institutional commitment, lenders underwriting risk, sponsors locking in structures, and projects transitioning from development to construction and, ultimately, operation.

It also represents a narrowing of execution risk. Markets do not deepen on announcements, they deepen on transactions.

While project finance represents only a portion of overall capital formation, its acceleration signals deepening institutional confidence and execution capability.

Execution changes market structure

Once assets move into operation, the nature of the market changes. Construction risk declines. Cashflows stabilise. This is when secondary markets begin to form organically.

Execution at scale enables:

- Stake sell-downs

- Portfolio-level transactions

- Refinancings and tenor extensions

The growth in new financial close activity today implies a larger universe of operational infrastructure tomorrow, and with it, greater capital recycling.

Risk compression expands the investor base

As track record builds, risk premiums compress. Documentation standardises. These shifts expand the pool of potential investors beyond large sponsors and state-linked institutions.

Execution maturity opens the door to:

- Mid-market infrastructure funds

- Specialist renewable platforms

- Regional family offices

- International capital previously constrained by perceived execution risk.

In effect, delivery credibility lowers the barrier to entry.

The next phase of Vision 2030

Saudi Arabia appears to be transitioning from capital mobilisation to capital velocity, where development capital is recycled into new projects, operating assets change hands, and balance sheets are actively optimised.

The data increasingly suggests that Vision 2030 is entering an execution led phase.

Over the coming years, this is likely to translate into:

- Greater secondary market activity

- Increased private-to-private transactions

- More complex refinancing and capital structuring

- A broader and deeper investor base

I regularly share observations on capital markets, infrastructure, and energy in Saudi Arabia. These views are my own and do not represent those of my firm.

Want to know more?