Belgian Tax Authorities’ position on OECD Pillar One – Amount B

14 April 2026

Tags

Transfer pricing

Simplifying the Arm’s Length Principle for routine marketing and distribution activities

Introduction

The Belgian Tax Authorities (BTA) recently published Circular 2026/C/45, an addendum to the existing Transfer Pricing Circular 2020/C/35. This circular clarifies the BTA’s administrative position on the application of the arm’s length principle by formally integrating the OECD’s ‘Pillar One – Amount B’ framework into Belgian practice. The framework is designed to simplify and streamline the pricing of routine marketing and distribution activities.

Applicable to transactions as from 1 January 2025, the framework introduces a standardized methodology for determining an arm’s length remuneration for in-scope activities, particularly in lower-capacity jurisdictions. While intended to reduce compliance burdens and enhance tax certainty, it also marks a significant shift in the pricing of routine distribution functions by moving towards a more formulaic, standardized approach.

Background

The introduction of Amount B should be understood in the context of the broader international tax reform developed by the OECD and the G20 under the BEPS 2.0 project. This reform is structured around a two-pillar approach aimed at addressing the tax challenges arising from globalization and the digitalization of the economy.

Pillar One focuses on the allocation of taxing rights and is divided into two components:

- Amount A targets the largest and most profitable multinational enterprises, reallocating a portion of residual profits to market jurisdictions where customers or users are located.

- Amount B has a more technical and operational focus, seeking to standardize the remuneration of routine marketing and distribution activities, which have historically been a frequent source of complexity and dispute in transfer pricing.

The rationale behind Amount B lies in the practical difficulties associated with applying the arm’s length principle to baseline distribution activities. Under traditional transfer pricing rules, determining an appropriate return typically requires detailed benchmarking studies under the Transactional Net Margin Method, often resulting in divergent outcomes across jurisdictions and prolonged discussions with tax authorities. These challenges are further exacerbated in jurisdictions with limited access to reliable comparable data and constrained administrative resources, leading to increased uncertainty and dispute risk.

To address these challenges, the OECD released its final guidance on Amount B in February 2024, incorporating it into Chapter IV of the OECD Transfer Pricing Guidelines. The framework introduces a simplified and standardized pricing mechanism, whereby qualifying entities may determine their return on sales by reference to a predefined matrix. This approach is intended to improve consistency of outcomes, reduce administrative burdens, and enhance tax certainty for both taxpayers and tax administrations.

Circular 2026/C/45

Circular 2026/C/45 follows the OECD framework including important clarifications that significantly affect how Amount B can be applied in Belgium. The BTA also indicate that any future amendments made to the 2024 OECD Report or its annexes (such as updates to the pricing matrix) will be accepted by the BTA. However, the BTA have introduced further clarifications:

I – Conditional application

The simplified approach is only accepted where all of the following conditions are met:

- The counterparty is located in a “covered jurisdiction” as defined by the OECD;

- Belgium has concluded a double tax treaty with that jurisdiction; and

- The jurisdiction has implemented Amount B in line with the OECD 2024 report.

In this context, “covered jurisdictions” are those that have politically committed to Amount B and for which Belgium agrees, in principle, to respect the outcome of the simplified approach. The list is maintained at OECD level and updated every 5 years. For ease of reference, the Appendix includes an overview of covered jurisdictions (with which Belgium has a double tax treaty).

To further clarify, the simplified approach is limited to cross-border intra-group transactions or dealings involving permanent establishments (and hence does not apply to purely domestic transactions).

II – Alignment with the OECD Guidelines

From a technical perspective, the Belgian circular aligns with the OECD report. This applies to:

- The definition of qualifying transactions (routine distribution, agents, commissionaires);

- The scoping criteria and quantitative thresholds;

- The exclusions (e.g. intangibles, services, commodities, complex risk profiles);

- The application of the Transactional Net Margin Method and the pricing matrix.

Rather than introducing additional local interpretations, the BTA confirm that these elements should be applied consistently with the OECD guidance.

III – Dispute resolution

The circular also provides important clarification in the context of dispute resolution.

In mutual agreement procedures (MAP) or arbitration, Belgium may accept an Amount B-based outcome on a case-by-case basis, but only where the counterparty jurisdiction:

- qualifies as a covered jurisdiction; and

- has implemented the simplified approach.

Where the counterparty jurisdiction does not apply Amount B:

- the simplified approach cannot be relied upon;

- the analysis reverts to the traditional OECD transfer pricing framework, as reflected in Circular 2020/C/35.

This underscores that the effectiveness of Amount B is highly dependent on consistent implementation across jurisdictions.

Recommended next steps

The Belgian implementation of Amount B represents a cautious but important step toward simplifying transfer pricing for routine distribution activities.

For businesses, the key takeaway is that Amount B is not a “one-size-fits-all” simplification. Its benefits will only materialize where jurisdictions are aligned and the eligibility criteria are met.

With the rules applicable as from 2025, businesses should act now to assess the potential impact on their transfer pricing policies.

Recommended next steps:

- Review existing distribution models and transactions against the Amount B criteria;

- Identify counterparties in covered jurisdictions (see Appendix). If your existing policy deviates significantly from the Amount B pricing, proactively evaluate the associated risks.

- Compare current policies and margins with matrix-based outcomes;

- Ensure robust documentation of eligibility, methodology, and outcomes, and reflect this where relevant in transfer pricing documentation (e.g. Local File).

We would be happy to assist you in assessing the impact of Amount B on your organization and in navigating the Belgian requirements.

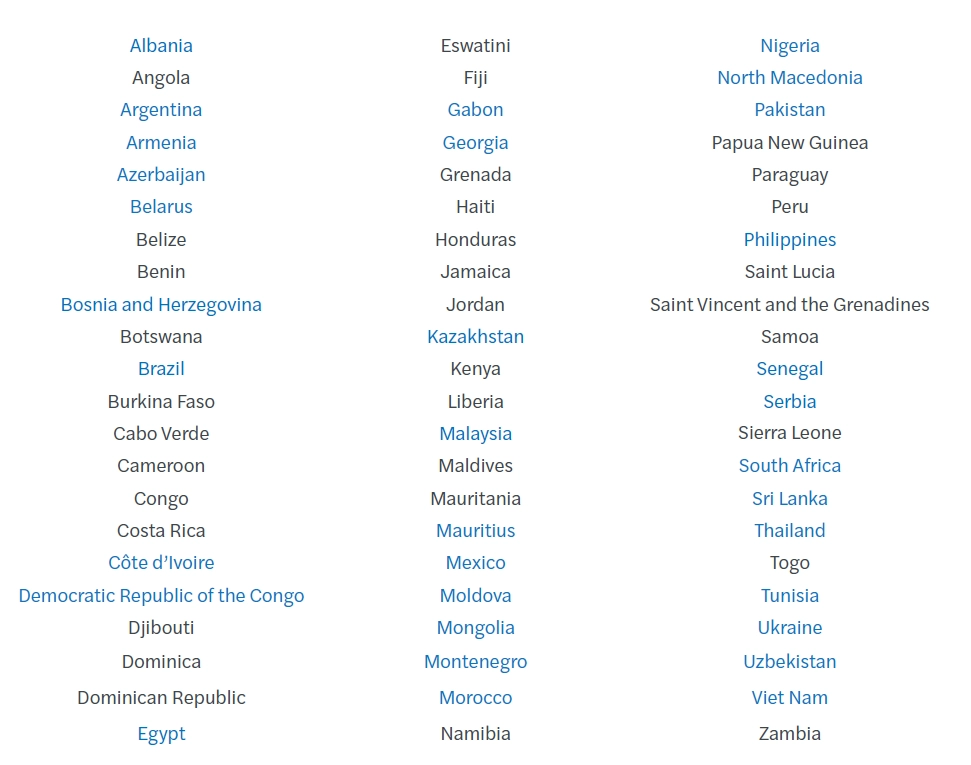

Appendix: OECD covered jurisdictions for Amount B (June 2024)

Below is the complete list of “covered jurisdictions” as defined by the OECD for the Inclusive Framework political commitment on Amount B. This list is updated by the OECD every five years, with the current iteration published in June 2024.

The countries highlighted in blue are those with which Belgium currently has an active Double Tax Treaty (DTT).

Want to know more?