Navigating global market conditions

InsightsC-suite barometerC-suite barometer: outlook 2026C-suite barometer: 2026 mid-year insights

Navigating global market conditions

4 June 2026

Fresh data from our mid-year C-suite barometer highlights the steadfast growth ambitions of businesses, the increasing complexities from ongoing uncertainty and the shift in how leaders are navigating global markets. Diversification is now the critical condition for growth in today’s climate, but diversification starts with pragmatism. Chief Economist George Lagarias explores the various market conditions driving businesses to diversify and examines the reality of this make-or-break strategy across various economies, industries and growth stages.

The global economy is resilient but fragile. This tension underpins many of the patterns seen in our mid-year data: continued optimism on growth alongside declining confidence in managing the external trends shaping that business growth.

What is surprising, and yet unsurprising, is the level of steady optimism – organisations will always back their ambitions. What’s more telling, is how leaders are rating market conditions both locally in their own countries and internationally, and this still shows strong favourability overall.

- 78rate local market conditions favourably

- 73rate international market conditions favourably

Responding to yesterday’s conditions, while preparing for tomorrow's uncertainties

One of the most important, and persistent, misconceptions in the boardroom is timing. Economic shocks do not play out instantly. So recent policy decisions, geopolitical disruptions and supply shocks are still working through the system.

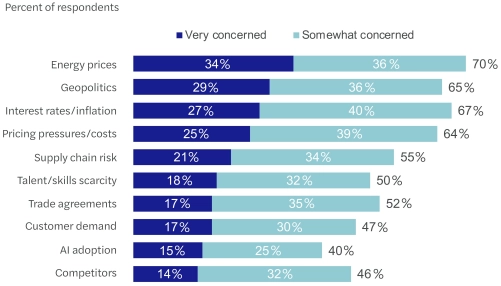

Concerns about global market conditionsAs inflation builds gradually, expectations become entrenched and only then do central banks respond – often tightening conditions just as growth begins to falter. This lag effect means leaders are frequently responding to yesterday’s conditions while preparing for tomorrow’s uncertainties. For boards, this creates a persistent strategic dilemma. It’s critical to identify whether what they are seeing now is temporary noise or the start of a more permanent shift. This is the only thing boards should be discussing – assessing whether structural change is underway or whether conditions will revert.

|

The consequences of inertia

At this point in the year, inertia can be the only key driver of the optimism we’re seeing. Consumers, businesses and markets tend to assume that the status quo will persist and that shocks are temporary. This behavioural bias sustains activity longer than expected but can also delay necessary strategic adjustments.

This distinction matters significantly for how leaders interpret diversification. What may appear as resilience or successful adaptation may in fact reflect delayed recognition of necessary or unavoidable structural change.

Diversification: strategy or default response?

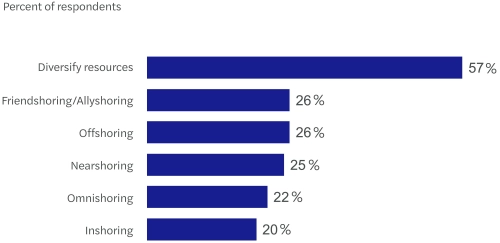

Against this backdrop, diversification has become a dominant response – across markets, supply chains, funding sources and operations. In fact, the last six months has seen a dramatic push to diversify resources in specific response to world events. It’s the top response in every region, with Latin America and Asia Pacific most likely to have accelerated. However, it’s important to recognise that the scale or approach to diversifying will be (and should be) different for every company. For some, expanding into new markets or broadening capabilities will strengthen resilience. For others, it introduces unnecessary complexity and risk. In some cases, the more effective strategy may be to outsource or deepen existing strengths rather than broaden exposure.

Operational change adopted/accelerated in the last six months, in response to geopolitical eventsThis reflects a deeper shift in how diversification should be understood. It is no longer about spreading risk indiscriminately, but about aligning strategic choices with core capabilities. In simple terms, executives must focus on what the company is really good at – for some, that might mean going back to basics or potentially streamlining its offerings. On a positive note, we saw some of this during the Covid-19 years with successful results. |

Introspection: the new strategic discipline

If there is one principle that should be prioritised above all others when going down the diversification route, and especially in uncertain times, it is introspection. In a fragmented and fast-moving global economy, the ability to assess internal strengths and vulnerabilities has become more important than any predefined strategy.

C-suite leaders and their companies need to do this regularly and this means understanding where earnings genuinely come from, identifying real competitive advantages, and confronting weaknesses without distortion. Essentially, introspection is what differentiates genuine adaptation from passive continuation.

Volatility is the new baseline

Perhaps the clearest message for C-suite leaders now, six months into the year, is that the current economic uncertainty and geopolitical volatility is not a transition back to stability – we need to get used to it (and this constant change) as the new norm.

There is no return to the great moderation and this has profound implications. It means that diversification strategies cannot be built on assumptions of stabilisation. Instead, they must be flexible, targeted and continuously reassessed against changing external conditions.

Short-term planning must reflect this reality too. For the next six months ahead, the guidance is pragmatic: monitor developments closely, reassess positioning constantly and ensure that the right people are in the right place – aligned to where the organisation holds genuine advantage and opportunity.

From diversification to disciplined decision making

Our mid-year data makes clear that diversification is shaping leadership agendas globally but the insight from this economic perspective is more nuanced and more demanding.

Diversification, on its own, is not a strategy. It is a tool. Its effectiveness depends entirely on context, capability and timing. In a world defined by constant lags in impact, persistent uncertainty and structural volatility, the leaders most likely to succeed will be those who diversify deliberately, remain grounded in rigorous introspection and clearly understand what is transient and what is permanent.

The challenge, as set out at the outset, is navigating global market conditions. The answer, increasingly, lies not in reacting to the environment, but in understanding the potential for what’s next – recognising the opportunities within it and having the confidence to adapt your approach quickly (and more regularly now, when needed) and act decisively.

Key contact

29 Jan 2026

C-suite barometer: outlook 2026

Our study uncovers a business world embracing change, investing in technology and people, and reimagining strategies to stay ahead of disruption and competition. Success now rests on adaptability as much as ambition.

4 Jun 2026

C-suite barometer: 2026 mid-year insights

At the start of the year, our C-suite barometer uncovered a business world embracing change, investing in technology and people, and reimagining strategies to stay ahead of disruption and competition. Six months on, the latest mid-year insights point to diversification as the defining condition for growth.