Corporate taxation in Korea and key considerations

24 April 2026

Tags

Tax

In general, a corporation's accounting year is determined in accordance with applicable law or the corporation's articles of incorporation. However, the period cannot exceed one year. If the accounting period is not specified, it can be selected during registration; without registration, the period is set to 1 January to 31 December.

Scope of corporation taxation

- Corporate tax law, income tax law

- Special tax treatment control law: corporation tax reduction and exemption related to the domestic source of income from foreign investment

- Tax treaties: limitation and modification of the application of domestic tax regulation

- Law for the coordination of international tax affairs:

- Transfer pricing taxation

- Limitation of interest deduction

- Tax haven taxation system

Tax residency

In general, taxable income is different according to the type of entity, as shown in the following table.

| Type of entity | Scope of taxable income |

|---|---|

| A resident or a domestic corporation | Worldwide income |

| Non-resident or non-domestic corporation with a domestic establishment (or permanent establishment) | All income related to the domestic establishment |

| Non-domestic establishment | The portion of domestic source income that is listed in tax laws |

A corporation with its head office, the main office, or a place of effective management within Korea is considered a domestic corporation. A corporation whose head office or the main office is located in a foreign country (on the condition that it does not own a place of effective management within Korea) is categorised as a foreign corporation.

Tax rate (including local income tax)

11%

Amount below KRW 200 million

22%

Amount exceeding KRW 200 million and below KRW 20 billion

24.2%

Amount exceeding KRW 20 billion and below KRW 300 billion

27.5%

Amount exceeding KRW 300 billion

Taxable income

| Type of corporation | Income for the business year | Capital gain | Scope of taxable income | |

|---|---|---|---|---|

| Domestic corporation | Profit corporation | All income from domestic and foreign sources | Subject to tax | Aggregate taxation |

| Non-profit corporation | Income from listed revenue-making business within domestic and foreign sources | Subject to tax | Aggregate taxation | |

| Foreign corporation | Profit corporation | Domestic source income | Subject to tax | Separate taxation (withholding tax or self-assessment) |

| Non-profit corporation | Income from the listed revenue-making business within the domestic source income | Subject to tax | Separate taxation (withholding tax or self-assessment) | |

Self-reporting system

Corporate taxation is a self-reporting system. A corporation with tax obligations must report and make the payment by self-assessment to the district tax office within three months following its business year-end.

Loss carried forward

Loss carried forward can be deducted for up to 15 years for the losses reported since 1 January 2021. In the case of small and medium-sized enterprises ("SME"), there is no limitation on the annual deduction amounts of loss carried forward. However, the maximum amount that can be deducted in a year 80% (effective for business years beginning on or after 1 January 2023) of the fiscal year's taxable income for non-SME taxpayers. For SMEs, a loss carried forward for a particular year can be retroactively applied to the most recent previous year's tax amount.

Consolidated taxation system

A domestic corporation and another domestic corporation (or "Completely Controlled Subsidiary") entirely controlled can apply for a consolidated taxation system by obtaining approval from the National Tax Service.

If there are two or more Completely Controlled Subsidiaries, all connected corporations shall adopt a consolidated taxation system. "Completley Controlled" means owning at least 90% of the shares. Within 5% of total issues shares, when the shares are held by employees through an employee stock ownership association, the association itself, or issued or transferred upon exercising stock options, the corporation is deemed "Completely Controlled."

Taxation of foreign corporations

The income of a foreign company branch is generally assessed in the same way and subject to the same tax rates as that of a locally incorporated subsidiary. In addition, certain foreign company branches can be subject to branch profit tax if the relevant tax treaty between Korea and the jurisdiction of the foreign company prescribes it.

Principle of substance over form

Principle of substance over form related to a transaction; a person to whom the transaction is substantially credited is a subject to the tax assessment. Principle of substance over form related to business contents: appropriate tax law is applied according to the substantial contents, disregarding its business title or form.

Limitation of interst deductions

In cases where a Korean subsidiary takes out a loan whose amount is twice as large as its equity (2:1 debt to equity ratio in general or 6:1 in the case of financial institutions) from its foreign controlling shareholder, the interest payable on the excess portion of the borrowing is disallowed and characterized as dividends. The deemed dividends are subject to withholding tax and treated as non-deductible expenses for corporate income tax purposes (Thin-cap rules).

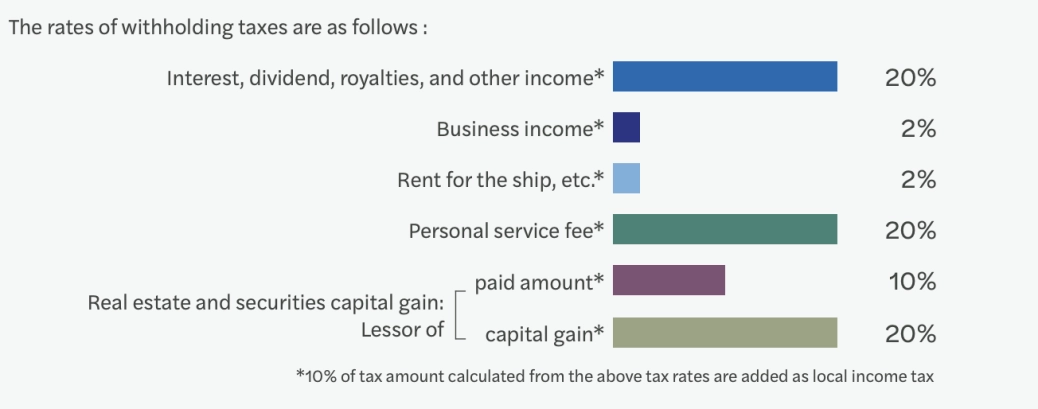

Withholding taxes

In the case of non-resident recipients, tax can be collected at the source. The Korean entity is required to withhold tax before paying or crediting specific categories of income to any non-resident recipient.

The above withholding tax rates may be mitigated where Korea has a double tax treaty with the recipient country. The withheld tax must be remitted to the Tax Authorities by the 10th day of the month following the month in which the non-resident was paid/credited. When failing to comply with the obligation, penalties are imposed.

Double tax treaties

Korea has an extensive network of double taxation agreements with other countries.

More about double tax treaties signed by the Republic of Korea

This article has been prepared based on selected content from the corporate taxation section of our guide ‘Doing business in Korea 2026.’

Want to know more?