Tax-free employee bonuses for 2026: Extensive administrative burden for limited tax exemption

It is furthermore noteworthy that the same cumbersome formal requirements are applied as were decisive for the employee bonus in 2024 (!!!) (see in this context § 124b no. 447 EStG as applicable at that time). Accordingly, for the tax exemption of employee bonuses in 2026, it is to be (once again) required that the payment is based on a wage-determining provision (“lohngestaltende Vorschrift”), whereby exclusively the following regulatory bases are recognized as such:

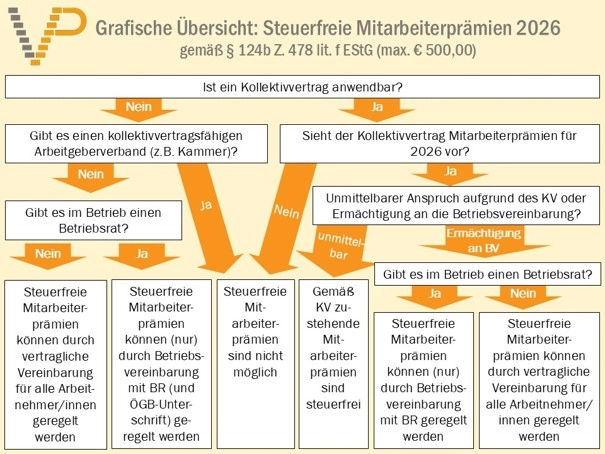

- Collective agreement (“Kollektivvertrag”);

- Works agreement (between employer and works council) concluded on the basis of an explicit authorization in a collective agreement;

- Works agreement (between employer and works council) where there is no collective bargaining–capable party on the employer side (in practice, this affects, for example, many associations), provided that the works agreement is co-signed by the competent trade union;

- In companies without a works council: an agreement applicable to all employees, provided that there is an explicit authorization in a collective agreement for regulation at company level or that a collective bargaining–capable party on the employer side is lacking.

The “regulatory monopoly” for tax-free employee bonuses in 2026 is therefore, as a matter of principle, intended to lie with the collective bargaining parties, i.e. the collective agreement either regulates employee bonuses itself (option 1) or provides an opening clause for a works agreement (option 2). Options 3 and 4 represent “collective agreement surrogates” in cases where there is no collective bargaining–capable employer association or no works council.

This means: If a collective bargaining–capable entity exists (thus, for example, in all companies that are members of the Austrian Federal Economic Chamber (Wirtschaftskammer), another chamber with collective bargaining capacity, or a voluntary employers’ association with such capacity), tax-free employee bonuses in 2026 can exclusively be enabled through a collective agreement. Consequently, if a collective bargaining–capable employers’ association exists but does not conclude a collective agreement on employee bonuses for 2026, tax-free employee bonuses will not be possible in 2026.

Link to the government bill for the Budget Measures Act 2026:

https://www.parlament.gv.at/gegenstand/XXVIII/I/504

Critical remark: The previous regulation for 2024 had already proven to be unnecessarily bureaucratic and had given rise to numerous interpretative issues and legal uncertainties. Against this background, it is difficult to understand why this unconvincing construct from 2024 is now being resorted to again. In addition, the attractiveness of employee bonuses for 2026 is further diminished by the significantly reduced tax benefit in quantitative terms. Although the legislative process still remains to be completed, no significant substantive changes to the government bill are to be expected.

The following decision tree is intended to assist in assessing whether tax-free employee bonuses for 2026 are feasible in a given company:

Der folgende Entscheidungsbaum soll bei der Beurteilung helfen, ob im jeweiligen Betrieb steuerfreie Mitarbeiterprämien für 2026 in Frage kommen oder nicht:

Figure source: Vorlagenportal.at