Personal taxation in Korea and key considerations

29 May 2026

Tags

Tax

In principle, a legal person with a tax obligation to pay for the income tax is an individual (resident and non-resident); however, in exceptional cases, a division, a foundation, and other organisations not classified as a corporation and an organisation considered as a resident or an organisation seen as a partnership have tax obligations to pay income taxes.

According to Korean tax law, a resident is an individual with a permanent home or domestic address who has resided there for more than 183 days, and a non-resident is an individual who is not a resident. The income tax law introduces a concept of “temporary residents” and acknowledges their limited tax obligations.

Range of taxable income

| Classification | Judgement standard | Tax obligation | |

|---|---|---|---|

| Resident | Permanent resident |

|

|

| Temporary resident |

|

| |

| Non-resident |

|

| |

Classification of income

The Korean tax law does not consider all income taxable and restrictively enumerates taxable income in a positive system.

Income classification:

1. Total income

- Interest income

- Dividend income

- Business income

- Wage and salary

- Annuity income

- Other incomes

2. Retirement income

3. Capital gain

Taxation system

Resident

The way for a resident to pay income tax is categorised as an aggregate taxation system, a separate taxation system, and a classified taxation system, based on its income type:

- Aggregate taxation system: calculating tax base and amount by aggregating all the income identified by its source (interest, dividend, business income, wage and salary, pension income, and other incomes)

- Separate taxation system (1): fulfilment of tax obligation as a way of withholding (among interest, dividend, not subject to separate taxation system (2) below, wage and salary, pension income, or other incomes, some incomes selected by the law)

- Separate taxation system (2): mandatory separate taxation on dividend income paid by high-dividend companies

- Classified taxation system: the income accumulated over a long period (retirement income and capital gain) falls under this system

Non-resident

A non-resident is only subject to pay income tax on a domestic source of income, and the determination of the applicable taxation system is based on its ownership of a domestic business place and the existence of realty rent income:

- Aggregate taxation system: a non-resident with a domestic business place or realty rent income is subject to tax according to the aggregate taxation system

- Separate taxation system: a non-resident without a domestic business place with interest, dividend, rent for the ship, etc., business income, personal service income, wage and salary, pension income, royalties, securities capital gains, and other income has to pay withholding tax as a means of fulfilling tax obligations according to the relevant double tax treaty

- Classified taxation system: in the case of retirement income and real estate capital gains, the process is identical with a resident to be separately categorised by the classified taxation system

Taxation period

In principle, the taxation period for income tax is from 1 January to 31 December of each year. If a resident is becoming a non-resident by moving their address or residence out of the country, the taxation period is from 1 January to the departure date for paying the exit tax.

Tax rates

The aggregate income tax rate is as follows:

| Aggregate income taxation standard | Tax rate* |

|---|---|

| Below KRW 14 million | 6.6% |

| KRW 14 million ~ below KRW 50 million | 16.5% |

| KRW 50 million ~ below KRW 88 million | 26.4% |

| KRW 88 million ~ below KRW 150 million | 38.5% |

| KRW 150 million ~ below KRW 300 million | 41.8% |

| KRW 300 million ~ below KRW 500 million | 44% |

| KRW 500 million ~ below KRW 1 billion | 46.2% |

| KRW 1 billion and above | 49.5% |

*Including local income tax equal to 10% of the tax amount

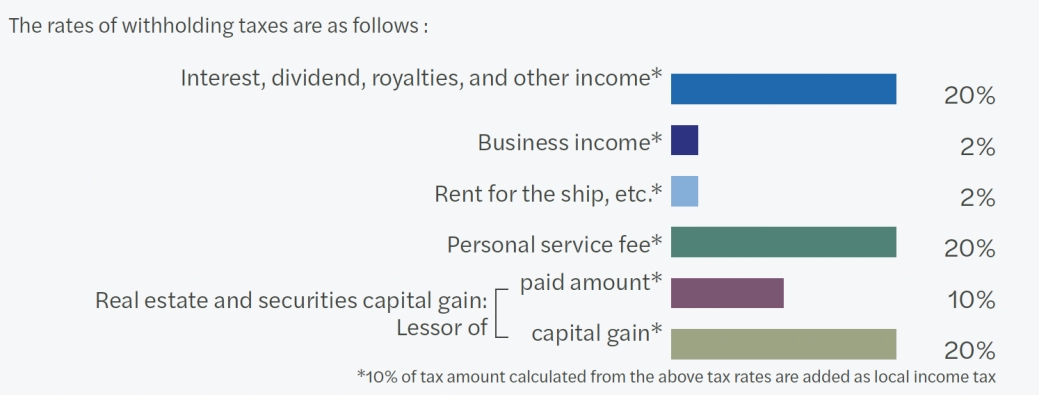

Withholding tax for non-residents

In the case of non-resident recipients, tax can be collected at the source. The Korean entity is required to withhold tax before paying or crediting specific categories of income to any non-resident recipient.

The above withholding tax rates may be mitigated where Korea has a double tax treaty with the recipient country. The withheld tax must be remitted to the Tax Authorities by the 10th day of the month following the month in which the non-resident was paid/credited. When failing to comply with the obligation, penalties are imposed.

This article has been prepared based on selected content from the corporate taxation section of our guide ‘Doing business in Korea 2026.’

Want to know more?