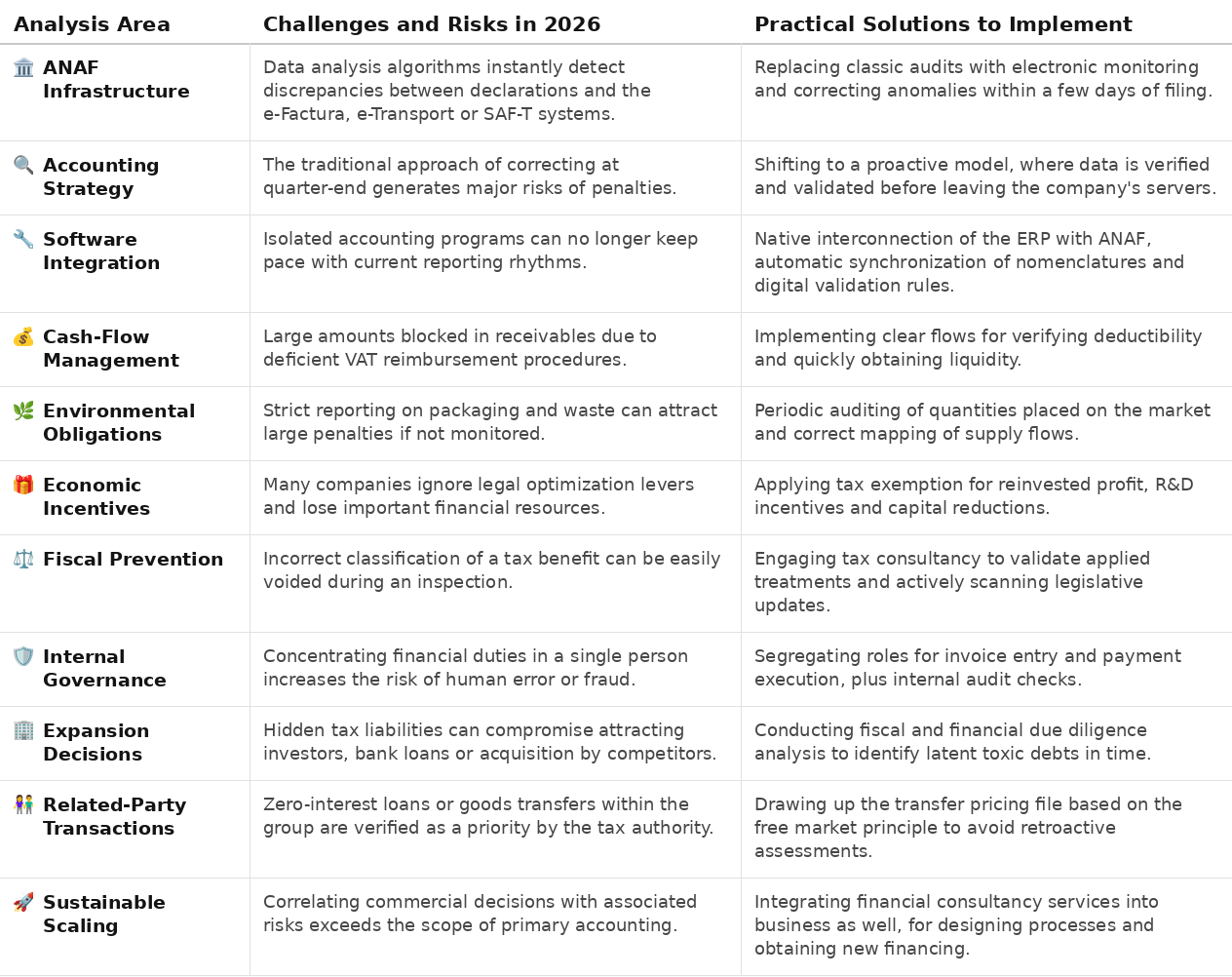

Digitalisation of tax reporting - from legal requirement to automated process in 2026

2026 marks the full maturation of the digital ecosystem implemented by the tax authorities. The relationship between SMEs and the tax administration has undergone a structural transformation, moving from periodic, retrospective checks to a continuous, automated flow of data. The RO e-Factura and RO e-Transport systems, together with complex reporting through the standard tax control file (SAF-T / Form 406), represent the daily operational pillars of any business.

The 2026 fiscal reality: the data analytics paradigm

Today, tax inspectors use advanced data analytics algorithms to scan, in real time, all the data reported by companies. This centralised digital infrastructure performs automatic reconciliations between invoices registered in the public system, declared movements of goods, and the detailed accounting data reported through SAF-T.

The direct consequence of this digitalisation is the immediate visibility of anomalies. Any discrepancy between the declared VAT base and the data extracted from e-Factura generates automatic alerts within the tax system. Traditional audits, carried out at the company's premises years after an error was made, are rapidly being replaced by electronic compliance notifications issued just days after returns are filed.

From reactive to proactive: the obligation of real-time accuracy

In this highly technology-driven landscape, the traditional approach of "we'll correct it at the end of the quarter" creates major compliance risks and exposure to penalties. An SME can no longer afford to treat tax reporting as a mere after-the-fact formality.

Important: financial and tax data entered into internal systems must be accurate from the very moment the transaction is generated.

The shift towards a proactive model requires implementing internal mechanisms to verify and validate data before it leaves the company's servers. A seemingly minor error in mapping product codes, or a delay in issuing an electronic invoice, instantly translates into non-compliance, directly affecting the risk indicators that the tax authority assigns to the company.

Optimisation through technology: integrating internal systems

To keep pace with the requirements of 2026, companies need a software architecture capable of automating reporting workflows. Simply using a standalone accounting programme is no longer enough, native interconnection between the internal ERP and ANAF's systems has become essential.

This is where the strategic importance of technology and digital solutions consulting comes in. Aligning IT systems with current legislation requires a dual skill set: a deep understanding of tax logic combined with technical IT configuration expertise. This process includes:

- Automatic synchronisation of internal nomenclatures with SAF-T structural requirements.

- Implementation of validation rules that block the transmission of erroneous data.

- Automation of download and reconciliation workflows for e-Factura, minimising human intervention and the risk of omissions.

Optimising cash flow and smart tax management in 2026

A mature tax strategy is not just about avoiding administrative penalties. Real financial performance lies in calibrating tax obligations in a way that protects and maximises the company's liquidity. In managing an SME, how taxes are administered directly influences the working capital available.

VAT and indirect taxes

Refunding and deducting Value Added Tax is often a major source of cash-flow pressure. Having significant amounts tied up in tax receivables due to inefficient procedures or a lack of proper supporting documents reduces a business's operational capacity.

To maintain optimal liquidity, implementing clear processes for verifying deductibility is essential. Transaction transparency and accurate VAT returns enable quick access to refund mechanisms with subsequent control, ensuring the capital injection arrives exactly when commercial activity requires it.

Environmental taxes

Contributions to the Environmental Fund have become a cost component with a direct impact on gross profit margin. Regulations on packaging, equipment waste or other specific substances impose extremely strict reporting obligations on importers, manufacturers and traders.

The absence of accurate monitoring of quantities placed on the national market leads to substantial penalties. Proper management involves periodically auditing environmental obligations and correctly mapping supply flows, thereby eliminating the risk of retroactive tax assessments by the authorities.

Tax incentives

A large proportion of SMEs fail to make use of the legal levers available for optimisation, losing out on significant financial resources. The legislation provides clear mechanisms for retaining profit within the company to strengthen equity.

Among the most effective tools for stimulating economic growth are:

- Tax exemption for profit reinvested in technological equipment, assets used in production, or software licences.

- Research and development (R&D) incentives, which allow additional deductions when calculating the tax result, or the application of special tax credits.

- Percentage reductions granted for maintaining a positive equity position, in accordance with legal provisions.

The role of strategic tax advisory

Correctly applying these benefits without creating collateral risks requires rigorous technical analysis. Incorrectly assessing a project's eligibility, or miscalculating the base for reinvested profit, can easily be overturned during a tax inspection.

The role of a specialised tax advisory division is twofold. On one hand, it acts as a prevention mechanism, eliminating the risk of disputes by validating all tax treatments applied in advance. On the other hand, it actively monitors legislative changes to identify the incentives applicable to the SME's unique profile, ensuring that no legitimate saving opportunity goes unused.

Risk management and preparing for the next stage of growth in 2026

The management seat of a rapidly expanding SME quickly becomes far more complex than during the start-up phase. Moving from a simple entrepreneurial model to a structure capable of scaling requires a major shift in perspective: taxation can no longer be seen merely as an administrative cost, but as a central element of risk management. In 2026, a company seeking major partnerships, favourable bank financing or external investors must, above all, demonstrate structural cleanliness in its figures.

Internal control and governance

As the volume of operations grows, the absence of clear procedures within the finance department creates major vulnerabilities. Internal control is an essential safety net for any SME seeking to avoid human error and fraud risks.

Consider the practical case of segregation of duties. When a single person within the company handles entering purchase invoices, reconciling bank statements and ordering payments, the likelihood of breaches increases exponentially. A simple oversight, such as paying the same supplier twice, or accepting an invoice with incorrect data, can tie up vital working capital. Clearly structured approval workflows and a periodic internal audit act as a first compliance filter, correcting anomalies before they are officially submitted to the authorities.

Why an impeccable tax history matters

When an SME decides to take a major strategic step, whether securing significant bank financing, attracting an investment fund, or acquiring a smaller competitor to consolidate its market position, balance sheet transparency becomes the company's calling card. Before any signature, a tax and financial due diligence review will reveal any hidden vulnerabilities.

Picture an SME in the process of acquiring another company. During the tax analysis stage, the consultants discover that the target company classified contracts with several external collaborators as independent services, even though those individuals were operating in a relationship of dependency (using the company's logistics, working fixed hours). The risk that the tax authority could reclassify these contracts and retroactively impose social contributions and penalties is a ticking time bomb. Identifying this latent tax liability allows the buyer either to renegotiate the final transaction price or to demand firm guarantees, avoiding the assumption of a toxic liability.

Transfer pricing: related-party transactions under the inspectors' microscope

A common trap for entrepreneurs running several parallel business lines is the management of transactions between their own companies. If an SME transfers goods, provides management services, or grants loans to another entity in which it holds shares, these operations fall directly under transfer pricing rules.

Tax inspectors place a high priority on assessing whether such exchanges comply with the arm's length principle. A classic example is lending to an affiliated company at zero interest or at a rate well below market levels. In the event of an inspection, the authorities will reject this treatment, adjust the lending company's financial income to market levels, and retroactively calculate additional corporate income tax plus late-payment surcharges. The transfer pricing file is no longer an obligation exclusive to multinationals - it has become the primary legal argument that a growing SME can use to justify and defend its pricing policy in the event of a tax assessment.

A multidisciplinary approach as a growth driver

No major business decision can be taken in isolation from its tax and financial implications. Sustainable scaling of a company requires close alignment between the entrepreneur's commercial vision and the technical rigour of the processes behind it.

Engaging specialised financial and business consulting services gives management exactly the competencies that go beyond basic accounting. Whether it's designing an internal control system suited to the company's new scale, preparing documentation to access new funding, or securing an important transaction, independent technical support transforms risk management from a legal obligation into a genuine competitive advantage.

Table: solutions for SMEs aiming for full fiscal compliance in 2026

Why choose to work with Forvis Mazars in 2026 for your SME's future?

Fiscal security and business scaling depend directly on the ability to anticipate risks and implement tailored solutions before legislative pressure causes operational disruptions.

In 2026, Forvis Mazars is redefining the concept of consulting through solutions built together with entrepreneurs, offering predictability and technical excellence in a fluid financial climate.

Global rigour anchored in 30 years of local expertise

Three decades of presence in the Romanian market give our team a deep understanding of the specifics and dynamics of local entrepreneurship. This cultural and economic insight is matched by access to a leading international infrastructure.

- Scale and qualifications: A local team of over 370 professionals and 12 partners coordinates projects in Romania, backed by a global network of 40,000 specialists across more than 100 countries and territories.

- Elite certifications: Our consultants hold internationally recognised accreditations in the field, including ACCA, CFA, CPA and CISA. This technical independence guarantees objective analysis and high-quality solutions for any sector.

An integrated approach: all resources in one place

For an SME, splitting tax advisory, accounting and audit services across multiple providers creates additional costs and communication gaps. An integrated, one-stop-shop approach eliminates these weak links, fully covering the needs of a growing company.

Our flexible portfolio includes comprehensive financial audit, tax, legal and accounting services. In addition, dedicated structures provide advanced expertise for complex business scenarios:

- Payroll and compliance: Romania hosts a centre of excellence supporting the global payroll practice through the innovative PayWorld and InControl digital platforms, streamlining internal processes.

- Specialist technical structures: Our clients have access to niche resources such as the SAP Hub, the IFRS Desk, ESEF reporting support, alongside dedicated IT audit and cybersecurity services.

Digital technology and proactivity in the face of legislative change

Tax compliance can no longer be achieved through traditional methods. Moving to fully automated processes requires native digital tools capable of ensuring the real-time accuracy of financial data.

Forvis Mazars invests continuously in cutting-edge technology solutions to improve the client experience and ensure compliance with the authorities' new requirements:

- Signals & Atlas: The Signals digital collaboration platform streamlines day-to-day interaction, while Atlas, our global audit platform, enables the mapping of best practices and the delivery of seamless, integrated audits.

- Dedicated tax compliance: The use of specific tools, such as our proprietary SAF-T reporting application and the VAT Hunter solution, eliminates compliance risks and secures tax deductions.

This proactivity is also reflected in the thought-leadership resources made available to the business community. Through strategic publications such as the Central and Eastern European Tax Guide 2026 and the global C-suite Barometer study, clients receive clear analysis of economic trends, enabling them to make sound long-term financial decisions.

Sustainability and responsibility, put into practice

Modern financial performance is closely linked to ESG (Environmental, Social, Governance) principles. Forvis Mazars manages its operations with social and environmental impact in mind, and is an active signatory of the United Nations Global Compact (UNGC).

- Diversity in management: Our team promotes an inclusive environment; women represent 78% of all professionals in Romania, 45% of the local leadership team coordinating the strategic plan, and 54% of the local executive board.

- Reduced environmental footprint: The company's headquarters holds top international certifications (BREEAM Excellent and WELL Platinum) and runs on 100% renewable energy.

- Community involvement: Social responsibility translates into concrete action: over 1,100 hours of volunteering and pro bono initiatives carried out by more than 230 employees, supporting educational and social projects alongside prestigious NGOs (United Way Romania, Mia's Children, Hope and Homes for Children).

As a result, the full transparency now required by the authorities through the new reporting systems leaves no room for retrospective corrections or "we'll sort it out at the end of the quarter" approaches. For an SME to operate smoothly in 2026, its internal systems need to become resistant to human error and capable of validating financial data in real time. This digital pressure can be seen either as a tax cost or, conversely, as the catalyst for a long-awaited internal restructuring.

In this sense, companies that choose to strengthen their software architecture and work with teams capable of delivering an integrated compliance strategy, through tax advisory tailored to the new rules, consulting for risk management, and financial advisory, to secure capital flows, will navigate this year with a clear competitive advantage: fast business decisions, grounded in reliable figures.

Disclaimer: This article is for informational purposes only and does not constitute professional advice.