Taxation of French real estate companies: What every Swiss resident needs to know

French SCIs can create complex Swiss tax consequences for residents holding rental property. Discover what the Federal Supreme Court ruling means in practice.

Many Swiss residents invest in French rental property through French “sociétés civiles immobilières”, commonly referred to as SCIs. However, the treatment of these structures by the Swiss tax authorities remains complex and subject to some uncertainty.

The Federal Supreme Court’s judgement of 13 December 2022 (2C_365/2021) concerning a case in the Canton of Vaud, served to clarify the Swiss tax treatment applicable to French SCIs in relation to wealth tax, though it also had the effect of introducing additional complexity.

This newsletter focuses solely on the tax treatment of SCIs holding rental property and therefore excludes SCIs holding property for personal use (main or secondary residences).

Swiss tax regime applicable to SCIs

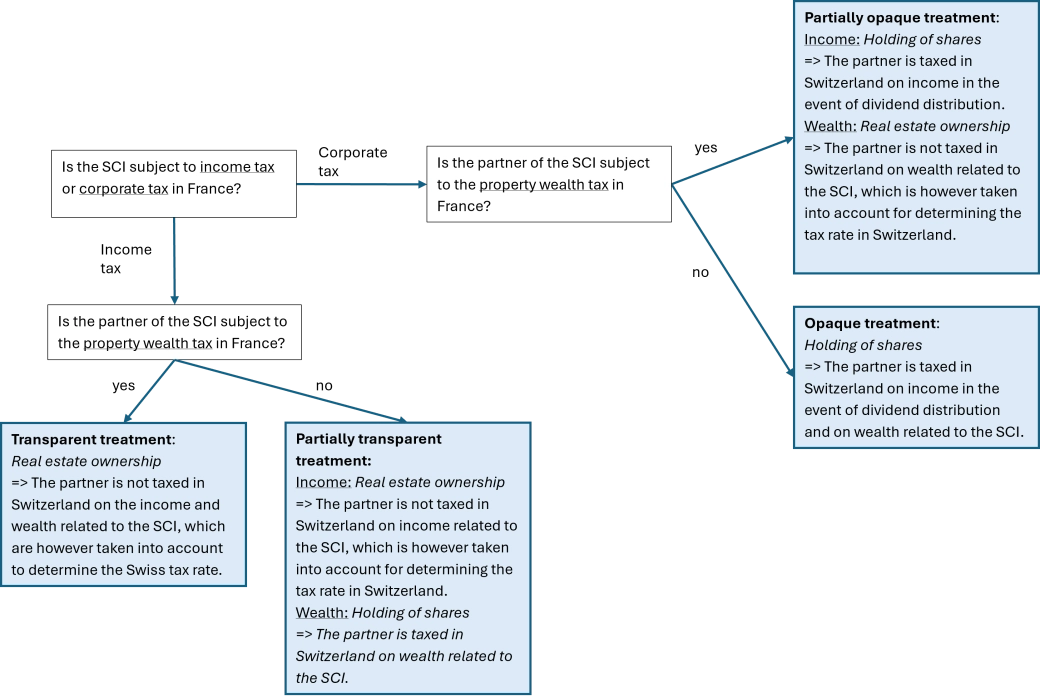

It should first be emphasised that SCIs are not companies governed by Swiss law and as such, are not recognised under Swiss commercial law. Consequently, the Swiss tax treatment applicable to SCIs depends on how they are treated for tax purposes in France. To determine this, the following two questions must be considered:

Is the SCI subject to income tax or corporation tax in France?

Under French regulations, SCIs may be subject to income tax or corporation tax in France. In principle, this is a choice left to the SCI’s partners. The tax treatment in Switzerland will therefore depend on the tax regime chosen in France.

Is French property wealth tax payable in relation to the SCI?

The Federal Supreme Court’s judegement clarifies that the Swiss wealth tax treatment of SCI shares now depends on whether the Swiss shareholder is personally liable for French property wealth tax (IFI). As a reminder, the IFI applies when the net value of French property assets, after deduction of debts, exceeds EUR 1.3 million.

Depending on the answers to these two questions, four distinct tax régimes may apply, as summarised in the diagram below.

It is important to note that the diagram represents a summary of our current understanding of the Swiss tax treatment applicable to SCIs following the publication of the Federal Supreme Court judgement. Nevertheless, we cannot exclude the possibility that certain cantons may apply specific rules in practice.

What should you do now?

- Ownership of an SCI involves significant tax complexity, with numerous factors to take into account. It is therefore essential to ensure that these investment structures are correctly handled and declared to the Swiss tax authorities. In this context, it is particularly important to: Determine or confirm the applicable Swiss tax regime for your SCIs based on your individual circumstances

- Review your Swiss tax return by correctly reporting the details relating to your SCIs in accordance with the applicable regime.

In the absence of a proper analysis and a correctly prepared tax return from the outset, the tax authorities may be led to adjust the taxable items relating to the SCI, whether or not this ultimately proves to be warrented. This carries the risk of litigation that is often lengthy, costly and burdensome.

Authors: Emina Husejnovic-Selimovic and Quentin Eiselé

Want to know more?