7.5% Tax Rate for creative practitioners

An optional flat rate of 7.5% is available on the first €50,000 arising from artistic activities conducted on a self-employed basis.

Do you have self-employment income arising from artistic activities?

This incentive provides the option to pay 7.5% tax on gross receipts before any deduction derived from an artistic activity by a creative practitioner. Those eligible are entitled to benefit from a tax rate of 7.5% on income from an artistic activity not exceeding the amount of €50,000.

Who is eligible for this incentive?

This incentive is eligible for those individuals who are self-employed on a full-time or part-time basis and the artistic income derived has been certified by the Arts Council Malta. Artistic income refers to income earned from:

- theatrical, stage, motion picture, and TV productions

- exhibitions

- paintings, sculptures, literary and musical works

- intellectual property, royalties

- project management

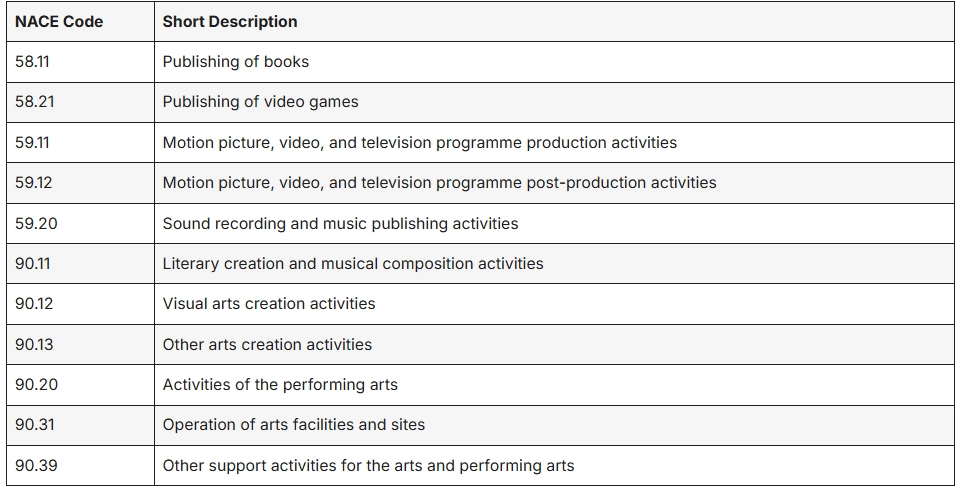

Eligible economic activities must be classified under one of the following NACE Code Rev 2.1 to be able to be eligible.

Your NACE Code is available on the Information Sheet attached to your VAT certificate. Should you have an earlier version of your NACE code, you are required to request a re-print of your VAT Certificate which will include the latest version of the NACE Code Rev 2.1.

It is essential to note that communication with the NSO is not proof enough for the purposes of this scheme. This scheme requires the VAT Certificate and the Information Sheet as proof of your NACE Code.

How to apply for the 7.5%?

If you are an artist in possession of the certificate of approval issued by the Arts Council, you can now opt to pay 7.5% final withholding tax on the first 50,000 earned, by declaring your gross income on the TA26 form. This form must be submitted by not later than 30th of April and needs to be accompanied by an approval issued by the Malta Arts Council.

The Certificate of Approval is issue by the Malta Arts Council (ACM). An application for such approval needs to be submitted by not later than 2nd April 2026 at noon and such application needs to be accompanied by the following documentation:

- Copy of the VAT Certificate

- Proof of the NACE code at Rev 2.1 classification

- Accountant’s Declaration.

How can we assist?

We can help you in assessing if the 7.5% tax rate is beneficial for you as well as providing you assistance with your compliance obligations. We can also assist you in preparing your personal income tax return as well as TA26 through which you can avail yourself of the 7.5% tax regime.

If you require further guidance or details in relation to this process, please do not hesitate to contact us so that we may assist you.

Want to know more?

Ruth Farrugia Tax Director - Birkirkara

Lorraine Camilleri Tax Manager - Birkirkara