Foreign Loan: Managing Cross-Border Borrowing in Vietnam

13 April 2026

Here's what every Finance expert in Vietnam needs to know about foreign loan compliance from SBV registration to tax implications.

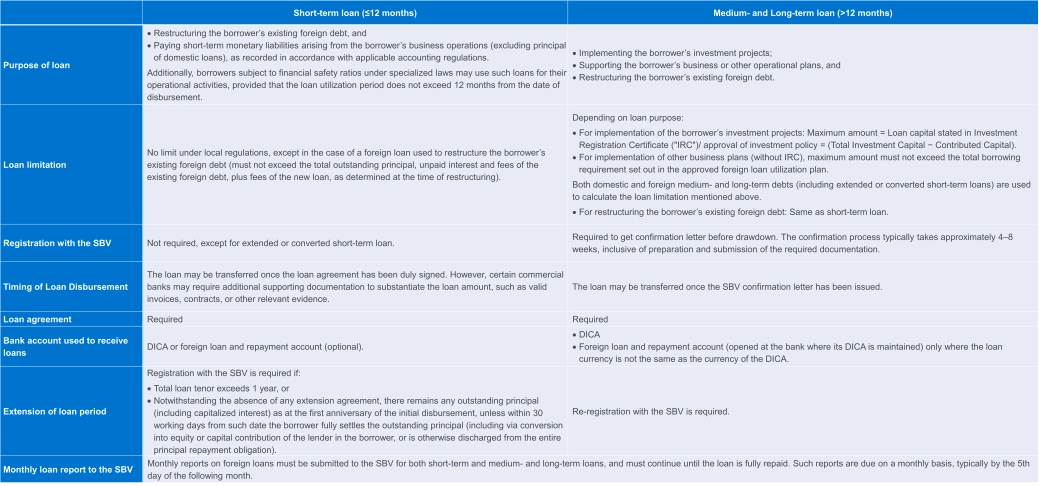

For many foreign-invested enterprises (FIEs) in Vietnam, borrowing from an overseas parent company or related party is a common and practical way to fund operations or capital expenditure. However, what appears straightforward on the surface can quickly become complex without the right knowledge of Vietnam's regulatory and tax framework.

The foreign loan must be structured correctly and properly from the beginning, to avoid further challenges down the road, such as being unable to repay the loan to the lender, administrative penalties imposed by the State Bank of Vietnam (“SBV”), or additional tax exposures. Below is a breakdown of what finance leaders need to know before proceeding.

Note on Loan Interest Rate

1. Civil transaction interest rate cap

For civil loan transactions, the interest rate may be freely agreed upon by the parties, provided that it does not exceed 20% per annum of the loan principal, unless otherwise stipulated by applicable laws (Article 468 of the Civil Code No. 91/2015/QH13, effective from 1 January 2017).

It should be noted that under SBV regulations, there is no official 20% cap on offshore loan rates. However, in practice, 20% serves as a "sensitive benchmark." During the registration of medium and long-term loans, the SBV may reject any all-in borrowing costs deemed excessive or indicative of transfer pricing. Any rate exceeding 20% may also trigger requests for justification from commercial banks.

2. Corporate Income Tax (CIT) Deductibility of Interest Expenses

For CIT purposes, where the Company has related party transactions, interest expenses are deductible only up to 30% of EBITDA (earnings before interest, depreciation, and amortisation). Accordingly, if the Company incurs high interest expenses but generates a low EBITDA, a portion of such interest expenses may be non-deductible when calculating CIT.

In cases where the Company records negative EBITDA in a tax year, the entire amount of interest expense may be treated as non-deductible for CIT purposes in that year.

Any non-deductible interest expense due to exceeding the 30% EBITDA cap may be carried forward and treated as deductible expenses in the subsequent five consecutive tax years, subject to the same 30% EBITDA limitation being applied in each of those years.

3. Withholding Tax (“WHT”)

Interest payments under the loan are subject to withholding tax (WHT). The applicable WHT rate on interest is 5% corporate income tax (CIT), with no value-added tax (VAT) imposed.

The loan agreement should clearly specify which party bears the WHT obligation in order to:

(i) determine whether the WHT is calculated on a net or gross basis; and

(ii) ensure that the WHT borne by the Company is treated as a deductible expense for CIT purposes.

4. Transfer Pricing

Interest expenses arising from related party loans are subject to transfer pricing risks, as they must be declared in the related party transaction disclosure submitted at year end. Accordingly, the applied interest rate should be consistent with market-based rates (arm’s length principle) to mitigate potential challenges from the tax authorities. Applying an interest rate of 0% may be viewed as inconsistent with market practice and could be challenged by the tax authority, may be imputed a deemed interest expense, which could trigger withholding tax (WHT) liabilities.

Key Takeaways

Setting up a foreign loan correctly from the outset is always more cost-effective than correcting it later. A well-structured arrangement, covering the right loan purposes and tenor, SBV registration timeline, bank account requirements, and tax positioning, ensures your company remains compliant and avoids unnecessary penalties or tax exposures.

Need help structuring your foreign loan in Vietnam?

If you are planning a foreign loan arrangement or need a review of your current structure, our Legal experts and Outsourcing experts are here to support you.

We help foreign-invested enterprises in Vietnam navigate cross-border borrowing with confidence, from registration to tax compliance.

Contact us

Dzung Dang Partner, Legal - Hanoi

Hang Doi Thi Bich Partner, Outsourcing - Ho Chi Minh City

Nhung Le Partner, Outsourcing - Ho Chi Minh City

24 Jul 2026

Circular 99/2025/TT-BTC

On 27 October 2025, the Ministry of Finance officially issued Circular 99/2025/TT-BTC ("Circular 99") providing guidance on the corporate accounting regime. The Circular has been effective since 1 January 2026 and applies to financial years beginning on or after that date. Vietnamese enterprises should now ensure that their accounting policies, systems and reporting processes reflect the new requirements.

6 Jul 2026

Vietnam's IFC:

Vietnam's International Financial Center is now backed by enacted law. See the legal stack, tax incentives, and how HCMC and Da Nang compare to global IFC hubs.

24 Jun 2026

Social Insurance refund for Expats

One often overlooked yet potentially significant benefit for foreign employees working in Vietnam is the lump sum Social Insurance refund. Despite its substantial financial value, this entitlement is frequently missed due to limited awareness and procedural complexity. With the right understanding and timely planning, expatriates may be able to recover a meaningful portion of their social insurance...

Update on on-the-spot import & export

On June 25, 2025, the National Assembly enacted a new law which introduces amendments to eight existing laws concerning finance, bidding, and investment. This law becomes effective on July 1, 2025.

3 Jun 2026

Valuation: Discounts and Premiums (2026)

Discounts and premiums translate differences in rights, liquidity, and information asymmetry into price. They should only be applied when the subject interest differs from the benchmark value you started with, such as guideline public multiples or a control-based DCF. Misapplying them is one of the most common, and costly, errors in business valuation.