Unlocking Vietnam's Venture Capital: Legal pathways, 2025 Regulatory updates & Ecosystem overview

22 April 2026

In April 2026, Ho Chi Minh City's People's Committee approved the establishment of a local venture capital fund with an initial charter capital of VND 500 billion (~USD 19 million). The announcement marks the first concrete application of Vietnam's newly established state-backed venture capital architecture.

This development is enabled by two landmark regulations issued in 2025. Resolution 198/2025/QH15 introduces targeted tax incentives across the innovative startup value chain. Decree 264/2025/ND-CP establishes, for the first time, a comprehensive legal framework for state-backed venture capital investment in Vietnam. Together, these instruments represent the most significant reform of Vietnam's venture capital regime in recent years.

This article examines the baseline legal framework, the 2025 regulatory updates, Vietnam's positioning relative to regional peers, and key considerations for investors and startups over the next 12 to 24 months.

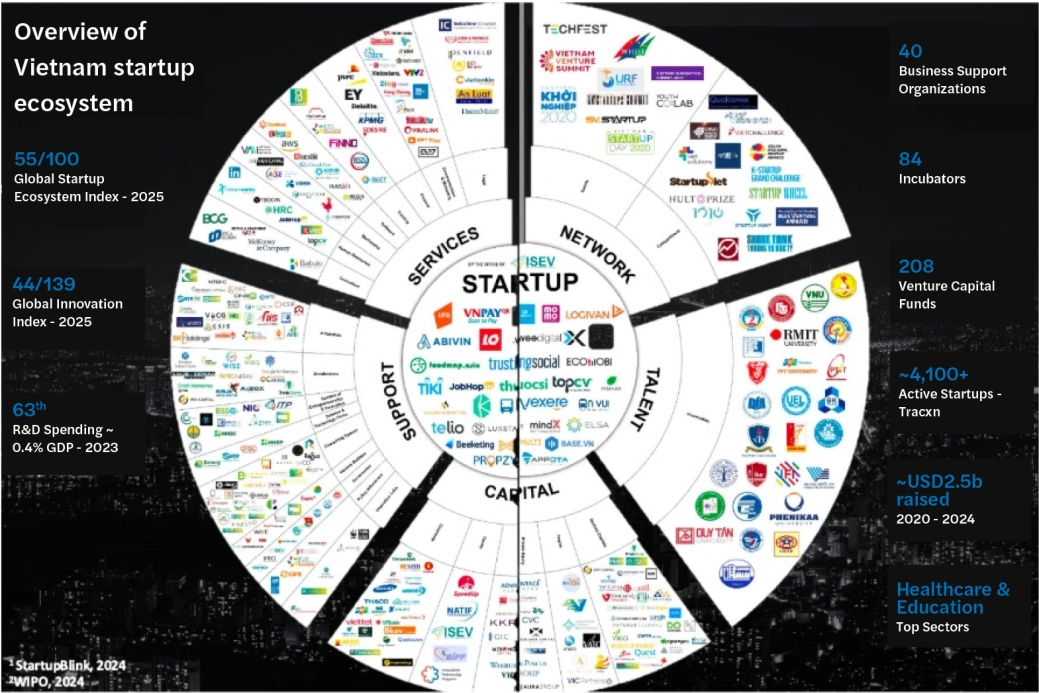

Vietnam's Startup ecosystem at a glance

Vietnam's venture ecosystem encompasses:

- 4,100+ active startups

- 208 venture capital funds

- 84 incubators and 40 business support organizations

- Approximately USD 2.5 billion raised between 2020 and 2024

Geographic concentration remains pronounced. Hanoi (~2,127 startups) and Ho Chi Minh City (~2,098 startups) dominate the landscape, while Da Nang is emerging as a secondary hub.

The macroeconomic context remains supportive. The Vietnam Innovation & Private Capital Report 2025 (VPCA and NIC, in collaboration with BCG) values Vietnam's digital economy at USD 36 billion in 2024 and a trajectory toward much larger digital contribution to GDP by 2030. The ecosystem is further supported by national platforms including TECHFEST, NSSC/NATEC, and the National Innovation Center (NIC).

Picture: Vietnam innovative startup ecosystem overview, NSSC

In this context, two key regulations were issued in 2025 that promise to provide tailwind for venture ecosystem in the next decades.

- Resolution 198 frames private sector development as a policy priority and includes measures touching on compliance burden and incentives that can affect startup formation and scaling conditions.

- Decree 264 set the formal structure for state backed venture activity alongside private VC pathways, following regional peers such as Singapore (SG Growth Capital), Malaysia (Cradle Fund + VentureTECH), Thailand (BOI matching fund + NIA co-investment).

Baseline legal framework for investment in innovative startups

The existing framework comprises the Law on Assistance for SMEs 2017 and Decree 38/2018/ND-CP. It governs investment in innovative startups through equity-based mechanisms. It also sets out the principles for State participation via indirect investment through selected startup funds.

After seven years of implementation, Decree 38 revealed practical shortcomings in the operational mechanisms of innovative startup investment funds. In July 2025, Decree No. 210/2025/ND-CP amended and supplemented Decree 38 with two key breakthroughs:

- Intangible assets, including intellectual property rights, technology, and technical know-how are now formally recognized as permissible capital contributions to innovative startup investment funds

- Beyond direct equity investment (capped at 50% ownership), funds may now invest via convertible instruments and share subscription rights

What tax and policy incentives does Resolution 198/2025/QH15 introduce?

Effective 17 May 2025, Resolution 198 concretizes Resolution No. 68-NQ/TW of the Party Central Committee on private sector development. It introduces special mechanisms to promote innovative startups in Vietnam, with a primary focus on tax incentives across the full startup value chain:

- Corporate Income Tax (CIT) incentives: Qualifying income from innovative startup activities benefits from a 2-year CIT exemption followed by a 4-year 50% CIT reduction. This applies not only to innovative startups but also to innovative startup investment fund management companies and supporting intermediaries.

- Capital transfer tax treatment: Personal Income Tax (PIT)/CIT exemptions apply to income from transfers of shares/capital (and related rights) in innovative startups, directly relevant to investor exit economics and secondary transactions, subject to implementation guidance and eligibility conditions.

- Policies on experts and human resources: A 2-year PIT exemption followed by a 4-year 50% PIT reduction applies to salaries and wages of experts and scientists working at innovative startups, strengthening talent attraction and retention conditions.

- Access to business premises: Priority allocation of production and business space, with at least a 30% reduction in land rental fees for the first 5 years.

What does Decree 264/2025/ND-CP establish for National and Local VC Funds?

Decree 264 establishes Vietnam's first formal state-backed VC architecture under the Law on Science, Technology and Innovation 2025:

- National VC Fund: Overseen by the Ministry of Science and Technology (MOST), with a minimum state capital allocation of VND 500 billion. Mandated for direct investment, co-investment, and fund-of-funds strategies, including overseas investment in innovative startups.

- Local VC Funds: Established by Provincial People's Committees with a domestically focused mandate, direct and co-investments within Vietnam only, without overseas or fund-of-funds activity.

- Socialization of the Funds: Both fund types seek to mobilize participation from domestic and foreign organizations and individuals alongside catalytic State funding. Fund managers may benefit from civil liability exemption and exclusion of administrative liability for investment losses, subject to conditions: losses must result from objective risks rather than intentional misconduct, with full compliance with applicable investment principles, internal regulations, and duties of transparency and good faith.

Both fund types operate under a strict risk framework: capital deployment terms of up to 10 years (extendable to 15 years), a hard 50% charter capital loss cap per cycle, and civil liability exemption for fund managers who fully comply with due diligence, transparency, and good faith obligations.

How does Vietnam's framework compare to regional peers?

Vietnam's new framework under Decree 264 is a first step. Several regional peers have been operating state-backed venture capital systems for years, and Singapore is already on its third generation. A brief comparison helps place Vietnam's position:

- Singapore (SG Growth Capital): On 1 April 2025, Singapore merged two existing state investors (EDBI and SEEDS Capital) into a single platform. It invests from seed stage through growth and strategic scaling. The Government always takes a minority position and lets the private sector lead each deal. No statutory loss cap has been publicly disclosed.

- Malaysia (Cradle Fund and VentureTECH): Malaysia's system is led by its Ministry of Science, Technology and Innovation (MOSTI) under the SUPER 2021-2030 framework. It supports startups from pre-seed through Series B, combining early-stage grants with later-stage equity and impact capital. Private capital participation is moderate and typically comes through sequential funding rather than formal matching.

- Thailand (BOI Matching Fund and NIA): Thailand offers matching grants of up to THB 20–50 million per startup, layered onto private venture capital rounds. The state only contributes after a private VC firm has already committed, and that firm must be on an approved list maintained by the National Innovation Agency (NIA).

What should investors and startups monitor over the next 12–24 months?

- For Resolution 198:

- Build a "tax incentive eligibility file" from the outset, covering IP ownership chain, R&D evidence, product novelty, growth metrics, and any government innovation status, because the payoff (capital gains and CIT/PIT exemptions) is meaningful but may be challenged if eligibility is unclear.

- Isolate and document eligible income streams early (contracting, invoicing, cost allocation) to avoid later reclassification risk. Note that inspection relief under Resolution 198 does not equal immunity, diligence on tax filings, e-invoices, labor contracts, social insurance, and related-party flows remains essential.

- For Decree 264:

- If syndicating with the National VC Fund or local VC funds, budget additional time for process and build term sheets capable of surviving committee review, with clear valuation logic, milestone-based tranches, governance rights, and downside protection.

- Treat co-investing with a state-backed fund like investing with a strategic LP. When syndicating, be prepared to present downside scenario analysis and structured governance that fits the fund's codified 50% loss cap risk narrative.

Ready to navigate Vietnam's venture capital framework?

If you are planning a venture capital fund structure, evaluating tax incentive eligibility under Resolution 198, or seeking to co-invest alongside state-backed VC funds under Decree 264, our Legal experts and Financial Advisory experts are here to support you.

We help innovative startups, fund managers, and foreign investors in Vietnam navigate the full legal and tax corridor, from fund establishment and investment structuring to compliance and exit planning.

📥 Download the full report below

Documents

Contact us

Hai Hoang Thanh Director, Financial advisory - Ho Chi Minh City

Dzung Dang Partner, Legal - Hanoi

24 Jul 2026

Circular 99/2025/TT-BTC

On 27 October 2025, the Ministry of Finance officially issued Circular 99/2025/TT-BTC ("Circular 99") providing guidance on the corporate accounting regime. The Circular has been effective since 1 January 2026 and applies to financial years beginning on or after that date. Vietnamese enterprises should now ensure that their accounting policies, systems and reporting processes reflect the new requirements.

6 Jul 2026

Vietnam's IFC:

Vietnam's International Financial Center is now backed by enacted law. See the legal stack, tax incentives, and how HCMC and Da Nang compare to global IFC hubs.

24 Jun 2026

Social Insurance refund for Expats

One often overlooked yet potentially significant benefit for foreign employees working in Vietnam is the lump sum Social Insurance refund. Despite its substantial financial value, this entitlement is frequently missed due to limited awareness and procedural complexity. With the right understanding and timely planning, expatriates may be able to recover a meaningful portion of their social insurance...

Update on on-the-spot import & export

On June 25, 2025, the National Assembly enacted a new law which introduces amendments to eight existing laws concerning finance, bidding, and investment. This law becomes effective on July 1, 2025.

3 Jun 2026

Valuation: Discounts and Premiums (2026)

Discounts and premiums translate differences in rights, liquidity, and information asymmetry into price. They should only be applied when the subject interest differs from the benchmark value you started with, such as guideline public multiples or a control-based DCF. Misapplying them is one of the most common, and costly, errors in business valuation.