Tax Transformation & Technology: Four steps to the next generation of tax functions

Who we areNewsPress & MediaNewslettersNewsletter „Steuern“Newsletter „Steuern“ 1/2026

The next generation of tax functions

Tax functions are currently at a turning point. Growing volumes of data, increasing transparency requirements and increasingly digital reporting and auditing processes are permanently changing the expectations of financial administrations, management and supervisory authorities. At the same time, tax risks and operational expenses are increasingly arising outside the tax department – along end-to-end business processes and in complex system and data landscapes.

Making a tax function fit for the future is more than just a technology project. It starts with a clearly defined target operating model, extends across processes, data and systems, and delivers added value where tax security, efficiency and transparency make a measurable contribution to the company's value creation.

Tax transformation therefore means strategically realigning the tax function as an integrated part of financial and business processes. It combines tax expertise with process, data and technology competence and creates the basis for data-driven control, automation and the effective use of modern technologies such as AI.

Clear structures for successful transformation

Our Tax Transformation & Technology (TTT) framework addresses this issue and provides guidance in a complex tax, organisational and technological environment. It structures the transformation of the tax function along clear development stages and combines specialist, procedural and technical expertise into a coordinated overall approach.

The starting point is the definition of a tax target operating model, on the basis of which processes and risks are analysed, documented, operationalised and automated. A particular focus is placed on the quality and integration of tax-relevant data, as this forms the basis for automation and the effective use of modern technologies such as AI. In this way, the framework supports a sustainable, resilient and future-proof tax function.

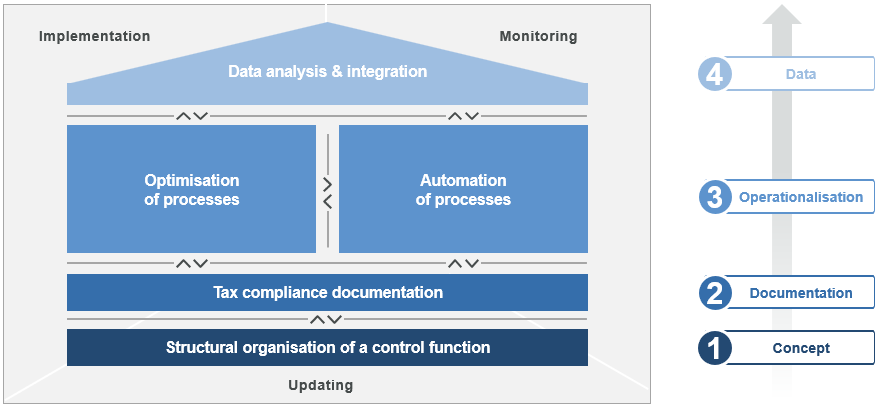

The TTT framework – four steps for the digital tax function

1) Design: In order to implement the diverse tasks and objectives of the company or the tax function, the organisation of the tax function within the company should be optimally structured and a clear target vision developed. When setting up a new tax function or further developing an existing one, several dimensions should be taken into account, including organisational structures, resource utilisation and potential for digitalisation. This results in our tax operating model.

2) Documentation: In order to ensure the complete, timely and verifiable fulfilment of all tax obligations, tax risks must be systematically identified, assessed and managed through clearly defined, process-oriented controls. On this basis, a company-specific tax compliance management system is developed, whose structured documentation reduces liability and penalty risks, increases transparency and data quality, and creates the basis for efficient and digitizable tax processes.

3a) Operationalisation/optimisation of processes: In order to integrate tax requirements effectively and sustainably into operational activities, it is necessary to take a consistent end-to-end view of tax processes. Since tax issues arise in upstream financial and business processes such as purchasing, sales, accounting and reporting, the focus is on defining and taking tax requirements into account within these processes. This optimises processes outside the tax function in a targeted manner, reduces risks and increases efficiency and process quality in the overall system.

3b) Operationalisation/automation of processes: In order to make tax and commercial processes sustainable, efficient, secure and scalable, consistent automation of key process steps is essential. GRC solutions enable system-supported monitoring and control of tax risks and controls, while optimised ERP systems, including API-based interfaces, enable automation across core and support processes. In addition, specialised software solutions and AI-based agent teams are used in the corporate ecosystem which, supported by RPA, handle core tax processes such as tax declarations, deadline management and regulatory requirements (e.g. DAC 6, Pillar 2) in a largely automated and integrated manner.

4) Data management: High data quality is crucial for data-driven tax risk management and the effective use of modern technologies such as AI. Hidden risks are identified through ERP-based mass data analysis and structured audit routines. A thorough analysis and structuring of the data and system landscape is essential, as only high-quality, integrated data forms the basis for automation and the efficient use of AI solutions.

Practical example: Automated VAT validation from ERP data

In many corporate groups, VAT-relevant data is generated in different ERP systems, countries and accounting areas. Divergent tax codes, inconsistent master data and different booking logics make consistent VAT compliance difficult. Manual spot checks or Excel evaluations are neither efficient nor sufficiently reliable for these data volumes.

Our TTT framework takes a systematic approach here: transaction data relevant for VAT purposes from the ERP system is transferred to a uniform, tax-interpreted data model and then validated automatically. Rule-based checks verify, among other things, the plausibility of tax rates and tax codes, the validity of VAT ID numbers and the correct application of reverse charge mechanisms. Any anomalies are promptly reported back to the relevant departments via workflow processes and documented in an audit-proof manner.

The result is scalable, data-based VAT compliance with higher quality, lower risks and a robust basis for further automation.

Our TTT framework: tax expertise meets practical technology

With its clear structuring of organisation, processes, automation and data, the TTT framework creates the conditions for a modern tax function. However, the full benefits of this transformation only become apparent when these elements are technologically integrated and effectively applied in day-to-day business.

This is exactly where our Digital Tax Portal (DTP) comes in. It is designed as a digital tax cockpit that centrally bundles and controls tax software, data analysis and AI-based applications. The DTP serves as an access point for tax applications and creates a uniform framework for analysis, validation, monitoring and automation.

The portal really comes into its own when combined with our clients' existing technology and data landscape. ERP systems, subsystems, reporting tools, connected data pools and data lakes are integrated via interfaces and made usable for tax purposes. The DTP thus functions as a tax integration and orchestration layer that enables end-to-end data and process flows and creates the basis for scalable automation and the targeted use of AI.

Conclusion: What does this mean in practice?

1. Get started quickly – know your own level of maturity

Getting started with tax transformation does not have to be a major project. The graphical representation of the TTT framework and the content described are useful pragmatic tools for realistically assessing the maturity level of your tax function. If you know where you stand, you can also see where to start.

2. Set priorities instead of doing everything at once

Based on these findings, the relevant areas of action can be prioritised. Not every tax function requires immediate automation or AI – but clarity about where risks arise and where there is potential for efficiency is.

The weak points are often already known: late filings, corrected tax returns, fines, penalties or recurring findings in tax audits are clear indicators that processes, data flows and technologies used need to be reviewed.

3. Sustainable implementation – with structure and technology

Those who take a structured approach and combine organisation, processes, data and technology in a manner create the basis for a resilient, future-proof tax function with measurable added value.

Contact