2026-2027 Australian Federal Budget tax & superannuation brief

The Treasurer announced the most significant set of tax changes in a Federal Budget in recent years, with substantial structural changes to the way investments and wealth are taxed. The changes for investors are coupled with several measures that are framed as providing favourable tax outcomes for individuals and businesses. Whilst these measures include many welcome changes, their impact will be much more limited than the tax increases for investors.

The most significant tax measures in the budget include the following:

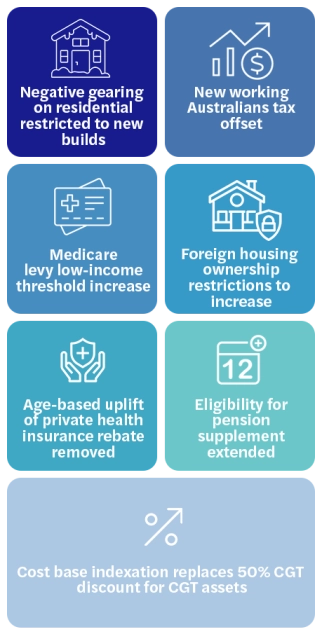

- Cost base indexation replaces 50% CGT discount

- Net capital gains will generally be subject to a minimum 30% tax rate

- Minimum 30% tax on trust distributions

- Double taxation for trust distributions to corporate beneficiaries

- Negative gearing on residential properties restricted to new builds

Additional key tax measures include the following:

- $1,000 Instant Tax Deduction and $250 Working Australians Tax Offset for workers

- FBT exemption for EVs to be phased down to a permanent 25% FBT discount

- Instant asset write-off of $20,000 for small businesses applying the simplified depreciation rules extended permanently

- Re-introduction of company loss carry-back rules for companies with up to $1 billion in turnover

- Small start-ups in their first 2 years of operation will be able to get a refund for tax losses capped to the value of employment taxes paid from 1 July 2028

- Changes to the R&D Tax Incentive rules that will increase rates and caps, but significantly reduce the scope of qualifying expenditure

Read ahead:

Download a PDF summary here

Individuals

CGT discount to be replaced with cost base indexation for all CGT assets from July 2027

From 1 July 2027, the 50% capital gains discount (CGT discount) will be replaced with cost base indexation for assets held for more than 12 months, with a 30% minimum tax on net capital gains applying from that date. This will apply to all CGT assets except new homes, including pre-CGT assets, held by individuals, trusts and partnerships.

The measure essentially restores the taxation of CGT assets by applying inflation-adjusted indexation based on the Consumer Price Index (CPI) to tax real gains. Indexation will be calculated using CPI similar to the pre-September 1999 method.

Existing assets purchased and sold before 1 July 2027 will still be eligible for the CGT discount. The CGT discount will also continue to apply to gains accrued until 1 July 2027 for assets purchased prior to that date, regardless of when the actual CGT event is triggered. The difference will be calculated by reference to the difference in the asset’s cost base and its value as at 1 July 2027.

Owners of new builds will be able to choose either the CGT discount or cost base indexation with the 30% minimum tax still applicable. Income support payment recipients, including Age Pension recipients are exempt from the minimum tax. New builds include dwellings constructed on vacant land, or where existing properties are demolished and replaced with a greater number of dwellings. Knock down rebuilds or substantial renovations are not considered new builds and therefore will not be eligible.

Negative gearing for residential property restricted from July 2027

Negative gearing for residential property will be limited to new builds and properties owned as at Budget Night from 1 July 2027.

Broadly, where net losses arise as a result of deductible expenses associated with income-producing property exceeding the income earned from that property, negative gearing allows the resulting net loss to be offset against other assessable income of the taxpayer.

Under the new measures, negative gearing arising in relation to residential properties will be limited to eligible new builds only. This means that investors in new builds will still be able to deduct rental losses against other assessable income, such as their salary. New builds include dwellings constructed on vacant land, or where existing properties are demolished and replaced with a greater number of dwellings.

The measure will apply to individuals, partnerships and most trusts. Widely-held trusts (eg most managed investment trusts) and superannuation funds (including self-managed superannuation funds) will be excluded.

Losses incurred from established residential properties will only be deductible against rental income or capital gains arising from residential properties. Any excess losses will be able to be carried forward and offset against income from residential property in future years.

These changes will apply to any established residential properties acquired from 7:30pm (AEST) on 12 May 2026. Any residential properties acquired prior to this time (including any contracts entered into but not settled) will be exempt from the changes until disposed of. Residential properties acquired between 7:30pm (AEST) on 12 May 2026 and 30 June 2027 may be negatively geared during this period, but not from 1 July 2027.

Commercial property and other asset classes, such as shares, will remain eligible for negative gearing. Exemptions to negative gearing will also be available for private investors who support government housing programs (through the provision of affordable housing).

New working Australians tax offset from 2027–28

Each working Australian taxpayer will receive a $250 Working Australians Tax Offset from the 2027–28 income tax year.

From 1 July 2027, the Working Australians Tax Offset (WATO) will provide a permanent annual tax offset for Australians for their income derived from work, such as wages and salaries and the business income of sole traders. It will increase the effective tax-free threshold for income derived from work by nearly $1,800 to $19,985 (or up to $24,985 for workers eligible for the low-income tax offset (LITO)). It will be paid automatically via workers’ tax returns at the end of the year.

The offset is in addition to the proposed $1,000 instant tax deduction for resident individuals who earn income for work from 1 July 2026 and the legislated 2025–26 Budget measure to reduce the personal income tax rates for individuals from 1 July 2026 and 1 July 2027.

Other measures for individuals

- Medicare levy: Low-income thresholds for singles, families, and seniors and pensioners will increase by 2.9% from 1 July 2025.

- Foreign ownership of housing: The temporary ban on foreign purchases of established residential property will be extended, alongside broader reforms to strengthen Australia’s foreign investment framework.

- Private health insurance: The age-based uplift to the private health insurance rebate will be removed from 1 April 2027.

- Pensions: Payment of the full pension supplement will be extended to 12 weeks for temporary absences overseas, with cessation for permanent overseas residents.

Trusts

Discretionary trusts to be taxed at minimum 30%

A minimum tax rate of 30% will be introduced on discretionary trusts from 1 July 2028.

Under current rules, beneficiaries are taxed on trust income distributed to them at their marginal rates, and any income accumulated in the trust is subject to 47% tax.

Under the new measure, trustees will pay a minimum tax of 30% (unless higher rates apply) on the taxable income of discretionary trusts (including capital gains) from 1 July 2028. Beneficiaries (other than corporate beneficiaries) will receive non-refundable credits for any tax payable by the trustee.

By excluding corporate beneficiaries from receiving a tax offset for tax paid by a trustee, distributions to corporate beneficiaries will effectively be double taxed. This will result a substantial change in the tax framework for family groups that utilise trusts and corporate beneficiaries.

Trustees will be required to calculate, report and pay the minimum tax, as well as to notify beneficiaries of their entitlements and associated tax credits. Trustees that receive franked dividends will be able to use their franking credits to pay the minimum tax.

The minimum tax will not be applicable to:

- other types of trusts (eg fixed trusts, unit trusts or widely-held trusts)

- complying superannuation funds

- special disability trusts

- deceased estates, and

- charitable trusts, and

- existing assets of testamentary discretionary trusts.

Some types of income such as primary production income, certain income relating to vulnerable minors and amounts to which non-resident withholding tax applies, will also be excluded.

Expanded rollover relief provisions will be available for 3 years from 1 July 2027 to support taxpayers that wish to restructure out of discretionary trusts to another entity type (such as a company or fixed trust).

Superannuation

Self-managed super funds provide an attractive wealth building refuge

There has been no change to how capital gains are taxed in superannuation funds, including self-managed superannuation funds (SMSFs). Superannuation funds (including SMSFs) will continue to receive a CGT discount of 33%. The 10% effective tax rate on capital gains in superannuation has now become (relatively speaking) even more attractive, and once a member is retired with their super in pension phase a zero tax rate will still apply if the member’s balance is below $2 million.

The disadvantage of superannuation is that the investor cannot benefit until they retire, but for those with a long-term investing view superannuation provides a low tax haven where profits can be compounded.

For those with superannuation account balances above $3million, the new Division 296 tax regime will apply from 1 July 2026. Now is the time for careful planning. Speak to your Forvis Mazars advisor and understand the impact of switching assets out of super in this new CGT environment.

Business

FBT exemption for EVs to be phased down

Australia will transition to a permanent 25% discount on FBT for certain electric vehicles (EVs).

From 1 April 2029, a permanent 25% discount on FBT will be available for all electric cars valued up to and including the fuel‑efficient luxury car tax (LCT) threshold, implemented through a 15% rate in the FBT statutory formula.

The following transitional arrangements will be adopted:

- all eligible electric cars will retain the FBT discount rate that was in place when the arrangement commenced

- all electric cars valued up to and including $75,000 that are provided before 1 April 2029 will continue to be eligible for a 100% discount on FBT, implemented through a 0% rate in the FBT statutory formula, and

- electric cars valued above $75,000 and up to and including the fuel‑efficient LCT threshold that are provided between 1 April 2027 and 1 April 2029 will be eligible for a 25% discount on FBT, implemented through a 15% rate in the FBT statutory formula.

Reportable fringe benefits will continue to be determined for eligible electric cars as if a 20% FBT statutory formula rate or cost basis method applied.

Small business depreciation — instant asset write-off of $20,000 made permanent

The instant asset write-off threshold of $20,000 for small businesses applying the simplified depreciation rules has been extended permanently from 1 July 2026. This measure finally resolves the perpetual extensions of the temporary $20,000 threshold over recent years and is a welcome change.

Under these simplified depreciation rules, an immediate write-off applies for low-cost depreciating assets. The current permanent threshold is $1,000, but this has been raised under temporary measures several times. A temporary threshold of $20,000 currently applies until 30 June 2026.

Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15% in the first income year and 30% each income year thereafter.

Company loss carry back rules re-introduced

From 1 July 2026 companies with aggregated annual global turnover of less than $1 billion will be able to use their current year tax losses to claim a refund for taxes paid in the prior 2 income years.

The loss carry back tax offset, was a previously introduced temporary measure applying from the 2019−20 to 2022−23 income years. Broadly, it allowed certain eligible companies to choose to carry back income tax losses incurred in those income years and apply them against their taxed profits in a previous income year. The benefit generated by this loss carry back was received in the form of a refundable tax offset that effectively represented the tax that the company would have saved if it had been able to deduct that loss in the earlier year.

The measure essentially re-introduces the loss carry back offset permanently for eligible companies and allows them to carry back tax losses and offset them against taxes paid up to 2 years earlier.

As with the previous temporary measure, the loss carry back tax offset will apply to revenue losses only and will be limited to the company’s franking account balance.

Loss refundability introduced for small start-ups

Small start-up companies that generate a tax loss in their first 2 years of operation will be able to utilise that loss to generate a refundable tax offset. The measure will apply for tax years commencing on or after 1 July 2028 to start-up companies with aggregated annual turnover of less than $10 million.

The offset will be limited to the value of fringe benefits tax and withholding tax on wages paid in respect of Australian employees in the loss year.

Reforms to R&D tax incentive

The Research and Development (R&D) Tax Incentive will be reformed to make it easier to use, increasing the incentive for new businesses to invest in eligible R&D activities.

From 1 July 2028, the measure proposes to:

- increase the offset for experimental “core” R&D expenditure from 25% to 50% through a 4.5 percentage point increase in core R&D offset rates

- remove the eligibility of supporting R&D expenditure for the R&D tax incentive

- reduce the intensity threshold from 2% to 1.5%, enabling more firms to qualify for higher offset rates

- allow greater access to the highest refundable tax offset for businesses younger than 10 years by increasing the turnover threshold from $20 million to $50 million, with an equivalent non-refundable offset available for eligible businesses older than 10 years

- lift the maximum R&D tax incentive expenditure threshold from $150 million to $200 million, and

- lift the minimum expenditure threshold from $20,000 to $50,000, with smaller R&D projects valued below $50,000 required to be undertaken with a recognised research organisation to support quality research outcomes.

Whilst framed as an increased incentive, the removal of eligibility of supporting R&D expenditure will materially decrease the expenditure base that will qualify for the R&D Tax Incentive. For many businesses claiming the R&D Tax Incentive, this will mean a reduction in benefits overall under these changes.

Other measures for businesses

- Venture capital: Expanded VCLP and ESVCLP thresholds from 1 July 2027, with closure of the eligible venture capital investor program to new applicants from Budget night.

- Global minimum tax: Amendments to Australia’s Pillar Two legislation will implement the OECD side-by-side package from 1 January 2026.

If you have any questions about how the Budget announcements may impact you, please speak to our Tax and Superannuation specialists.

| Melbourne - +61 3 9252 0800 | Sydney - +61 2 9922 1166 |

Evan Beissel Michael Jones | Lauren Hill Stephen Baxter Gaibrielle Cleary Jeremy Mortlock |

Published: 13/5/2026

Please note that this publication is intended to provide a general summary and should not be relied upon as a substitute for personal advice.

All rights reserved. This publication in whole or in part may not be reproduced, distributed or used in any manner whatsoever without the express prior and written consent of the Forvis Mazars, except for the use of brief quotations in the press, in social media or in another communication tool, as long as Forvis Mazars and the source of the publication are duly mentioned. In all cases, Forvis Mazars’ intellectual property rights are protected and the Forvis Mazars Group shall not be liable for any use of this publication by third parties, either with or without Forvis Mazars’ prior authorisation. Also please note that this publication is intended to provide a general summary and should not be relied upon as a substitute for personal advice. Content is accurate as at the date published.