Large European banks included in the sample maintain their resilience despite geopolitical risk and increased market volatility.

Our latest IFRS 9 benchmark study analyses the expected credit loss (ECL) levels and their changes for 26 large European banking groups, including two Irish banks, based on their 2025 annual reports published before 1 April 2026.

It examines the impact of ECL charges on profitability, movements in ECL allowances and coverage ratios, the allocation of exposures between IFRS 9 stages, the use of post-model adjustments and Banks’ approaches to the macroeconomic scenarios used in forward-looking information.

Overall, Irish banks are in line with the stable trend represented across European peers.

Key insights from Irish banks

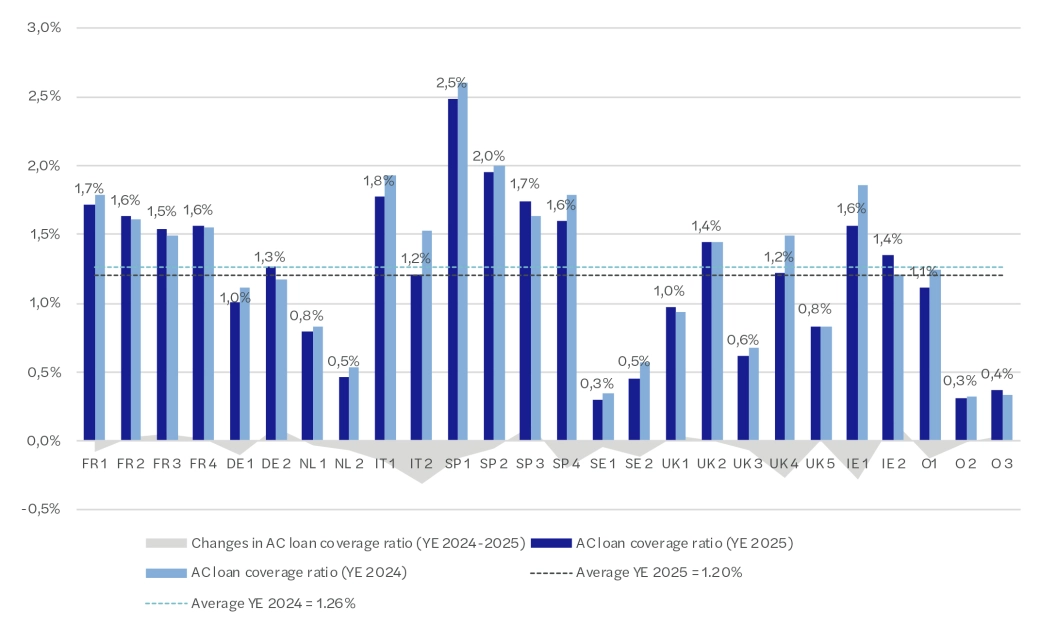

- Slightly higher AC coverage ratios in Irish banks (1.4% and 1.6%) in comparison to the average for the European banks (1.2%).

AC loans coverage ratio YE 2025 vs YE 2024

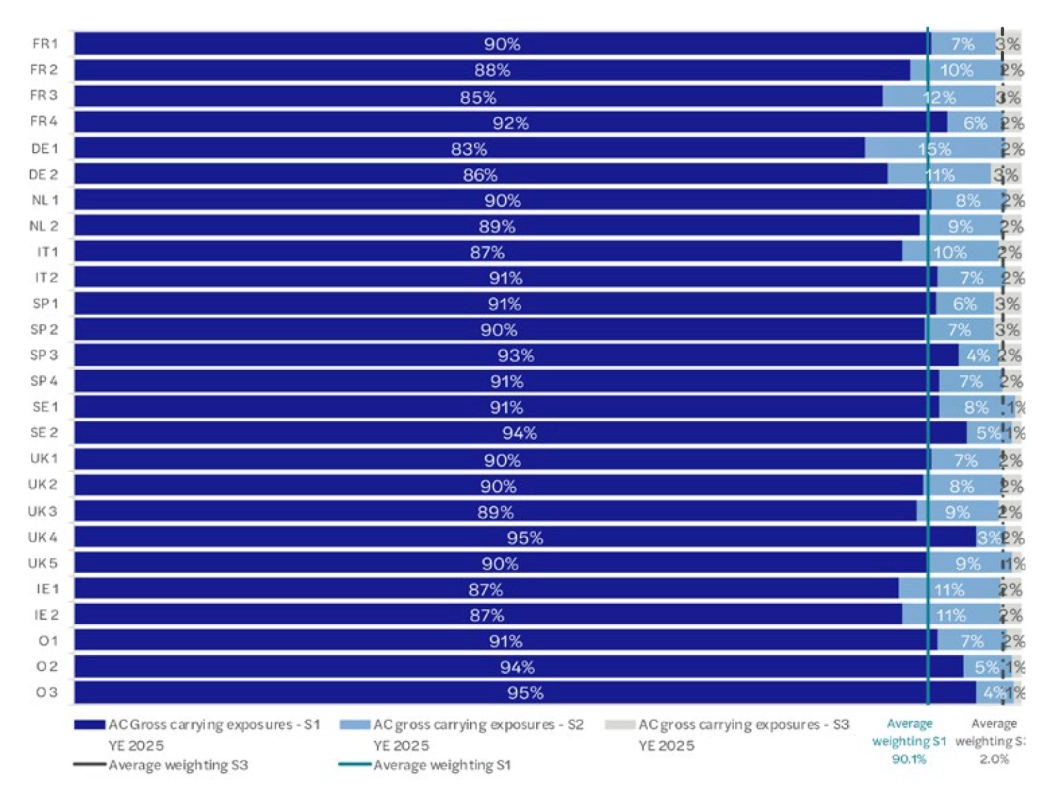

- Consistently higher proportion of exposures classified to Stage 2 and ECL carried by Stage 2 exposures in Irish banks vs European peers.

Allocation by stage of AC loans gross carrying exposures in YE 2025

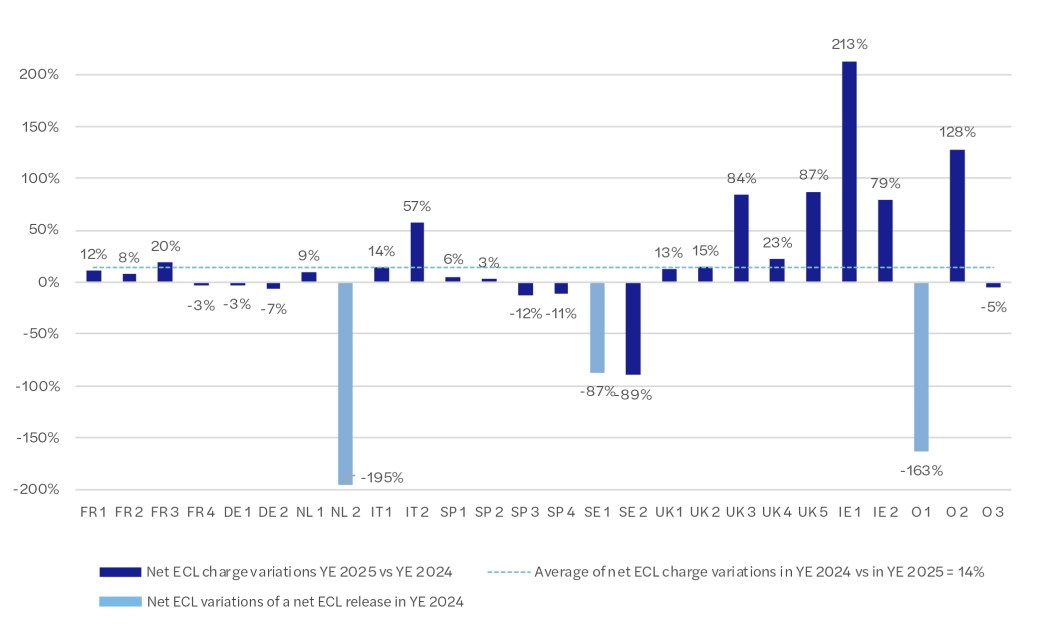

- More volatility in the YoY changes in ECL charge/release exhibited by Irish banks vs European peers.

Changes in ECL charge and release Var. YE 2025 vs YE 2024

Key insights from the whole sample

- The average coverage ratio for amortised cost (AC) loans fell to 1.2%, compared with 1.26% in 2024 and 1.57% in 2019.

- Stage 1 coverage ratios decreased across the sample while Stage 2 and Stage 3 coverage ratios increased slightly on average.

- Banks’ forward-looking scenarios continue to reflect caution, with downside scenarios weighted at or above 20% by most banks in the sample. These scenarios mainly account for the macroeconomic uncertainty and geopolitical risks.

- Post-model adjustments and overlays continued to decline, representing only 9% of amortised cost loan ECL allowances in 2025, compared with 10% in 2024.

- The average ECL charge increased by 14% year-on-year while its average share of operating profit before ECL remained broadly stable at 13%.