Nine years of GST: Simplifying taxation, strengthening India

Tags

Tax

VAT and indirect tax

Insights

Thought leadership

"Ek Bharat Shreshtha Bharat"

A look at how the tax base has grown, what GST 2.0 means for businesses, and where the reform still has work to do.

When the Goods and Services Tax rolled out on July 1, 2017, it promised to turn India's fragmented indirect tax map into a single national market. Nine years on, as the country marks GST Day 2026, the government's own assessment is unambiguous: "One Nation, One Tax" has moved from a slogan to a functioning reality, with the tax framework strengthening India's vision of Ek Bharat–Shreshtha Bharat over the past nine years.

Replacing a maze with a single framework

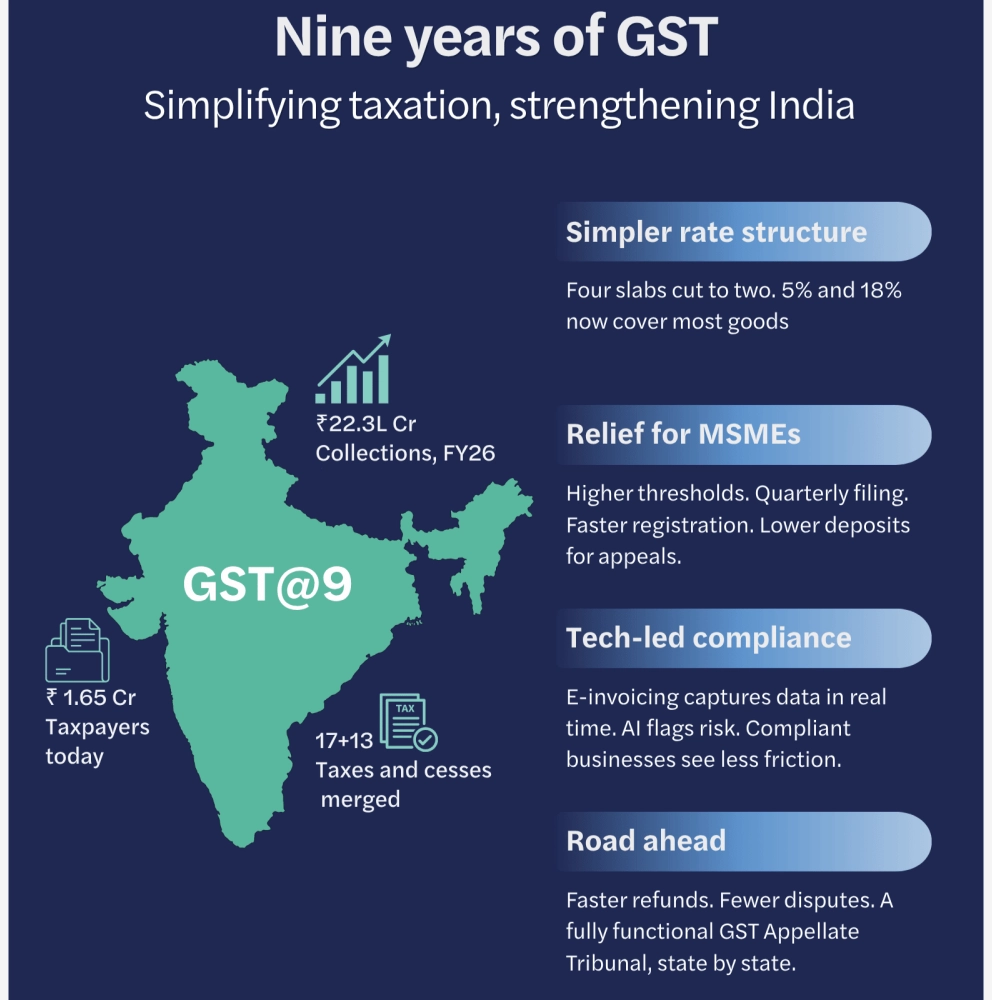

GST folded 17 different taxes and 13 cesses into one common framework, doing away with a system where multiple Central and State levies created inconsistent rates and structures, added hidden costs for trade and industry, and produced a cascading "tax on tax" effect. A strong IT backbone was built alongside this shift, aimed at widening the tax base and improving tax discipline across the country.

The architecture that emerged rests on a few defining principles. Tax is levied on the "supply" of goods or services rather than on manufacture, sale or service individually. GST is also a destination-based consumption tax, meaning revenue accrues to the state where goods or services are consumed — a design that inherently favours consuming states and reduces the scope for tax-driven distortions in where businesses choose to locate. Coverage is near-universal, with only alcoholic liquor for human consumption kept outside its scope, and the system applies common rates uniformly across the country.

Institutionally, the GST Council has been central to keeping the system responsive. As a statutory body bringing the Centre and states together in decision-making, the Council has strengthened cooperative federalism by regularly reviewing issues and enabling timely course corrections. Backing this is the Goods and Services Tax Network, a company equally owned by the Centre and states, which provides the shared digital infrastructure supporting taxpayers and administrators alike.

GST 2.0: the next generation reset

The most consequential recent shift came from the GST Council's 56th meeting. The Next-Gen GST reforms, effective from September 22, 2025, and branded GST 2.0, revised rates and exemptions with the explicit aim of improving the lives of common people and simplifying tax processes for businesses.

Three changes stand out. The rate structure has been streamlined largely into two slabs — 5% and 18%. A 40% rate has been carved out for luxury and sin goods such as lottery and online gaming, tobacco, aerated drinks, high-end cars, yachts and private aircraft, intended to protect revenue while making the overall structure fairer. And compliance itself has been eased — registration and return filing are simpler, refunds are faster, and costs are lower, with particular benefit to MSMEs and startups.

Beyond rate cuts, GST 2.0 is designed to lower costs, improve affordability and widen its sectoral reach, with households seeing cheaper goods and services alongside GST exemptions on insurance and essential medicines that strengthen access to healthcare. For industry, reduced rates on inputs such as cement and on sectors like handicrafts are expected to lower production costs, while a simplified structure should reduce classification disputes and gradually expand the tax base. Correction of inverted duty structures is also expected to boost domestic value addition and support exports.

Built-in relief for small taxpayers

A less discussed but steady thread through GST's nine years has been calibrated relief for smaller businesses. The registration threshold for goods suppliers was raised from ₹20 lakh to ₹40 lakh effective April 2019, while the composition scheme limit rose from ₹75 lakh to ₹1.5 crore in most states. The Quarterly Return Filing and Monthly Payment (QRMP) scheme, introduced in 2020, allows taxpayers with turnover up to ₹5 crore to file quarterly, and taxpayers with no transactions can file NIL returns via SMS. Small intra-state sellers on e-commerce platforms were exempted from mandatory registration from October 2023, and a low-risk applicant category now allows registration within three working days. On the dispute side, the pre-deposit required for filing GST appeals has been reduced, and interest and penalty waivers have been offered on certain demand notices for FY 2017-18 to 2019-20.

The numbers behind the formalisation story

Government data frames GST's growth as much a story of formalisation as of revenue. The number of GST taxpayers has grown from 66.5 lakh in 2017 to 1.65 crore as of May 2026 — a signal, in the government's reading, of a steadily formalising economy. On collections, gross GST revenue stood at roughly ₹7.4 lakh crore in 2017-18 and has climbed since, rising from about ₹13.76 lakh crore in 2021-22 to around ₹22.27 lakh crore in 2025-26, with momentum carrying into FY27 as April-May 2026 collections touched close to ₹4.37 lakh crore.

Underpinning this is a shift toward technology-driven administration, where the GSTN portal and e-invoicing enable real-time capture of invoice data, cutting manual reporting and reducing mismatches, while automated matching of supplier liability with recipient input tax credit has streamlined filing. Artificial intelligence, machine learning and data analytics are now used to flag possible evasion by analysing patterns and risk indicators across registration and scrutiny processes, allowing the system to focus scrutiny on high-risk taxpayers while easing the burden on compliant ones.

The road ahead

The government frames GST Day as more than a commemoration — it positions the reform as part of a continuing effort toward a simpler, more transparent, integrated indirect tax system, with GST 2.0 built to address citizen and business needs while supporting India's progress toward a Viksit Bharat.

For businesses tracking the policy trajectory, the signal is clear: after nine years of building the plumbing — registration, invoicing, return filing, dispute resolution — the government's stated priority is now to make the system lighter to carry, not just wider in reach. How consistently that translates into faster refunds, fewer disputes and a fully functional appellate structure will likely define how GST's second decade is remembered.

The write up is based on secondary research and PIB note.