Sign up to hear more from us

Select your interests and receive our latest insights, event invitations, news and more.

Unlike other risks, such as climate change, which will materialise in the medium to long term, cyber incidents are already having a significant adverse impact on some insurers. Despite this, cyber risk is less frequently mentioned in annual reports compared to climate change. We explore the importance of cyber risk disclosures and offer you practical tips on maintaining proportional and specific disclosures without increasing volume.

Insurers today face the dual challenge of paying out for cyber-related claims while also being targets of cyber-attacks.

The financial industry, including insurance, ranked second in spending on the tackling of data breaches in 2024 [1]. Increased online sales and AI usage have heightened insurers' exposure to cyber risk. Even large insurers with robust digital security can be vulnerable. For instance, Prudential's 2023 annual report revealed that the widely reported MOVEit data breach affected over two million customers and employees. Cyber-attacks can lead to various adverse events for insurers, including business interruption, loss of sensitive data, potential loss of funds aimed to cover insurance liabilities, reputational damage, and potential regulatory fines.

Meanwhile, cyber risk more broadly also presents underwriting opportunities, but exploiting these opportunities is not without its challenges. Despite mitigation efforts, claim frequency keeps rising. In the first half of 2023, cyber claims notifications increased, with third-party data breaches and ransomware being the main culprits [2].

Managing routine claims is part of insurers' core capabilities, but certain types of cyber claims pose new challenges. One such challenge is forecasting catastrophe cyber risk and assessing loss exposure, which involves significant uncertainty. Beazley's 2023 annual report mentioned the issuance of the first publicly traded cyber risk catastrophe bond, providing indemnity against all perils exceeding a $300 million catastrophe event. They forecast that supply chain attacks along with phishing followed by malware attacks, can cause cyber catastrophe events with loss ratios around 250% and 200%, respectively [3].

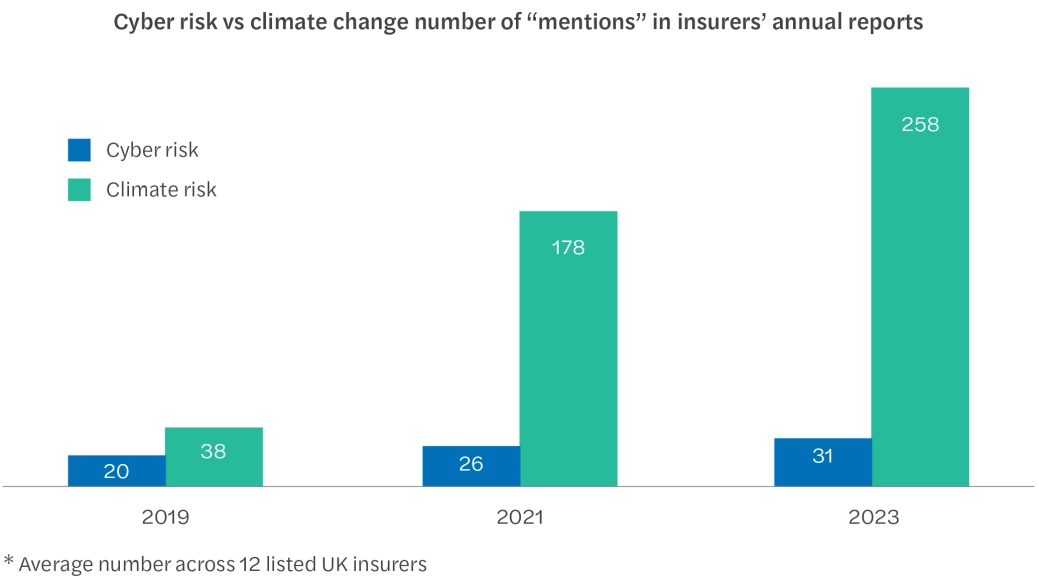

The mismatch between the high level of cyber risk and how it is disclosed in annual reports might cause concerns around insurers’ resilience. In 2023, UK LSE-listed insurers mentioned cyber risk an average of 31 times in their reports, compared to 258 mentions for climate risk. This is despite many insurers considering climate risk as either immaterial or a medium to long-term issue, while cyber risk could result in adverse events today and, like climate, requires a long-term strategic impact assessment, too.

A greater focus on climate change is understandable and directly linked to evolving climate regulation. The chart above shows a significant increase in mentions of climate change in 2023 compared to 2019, reflecting the introduction of FCA requirements for climate-related disclosures. While UK-listed entities must disclose climate risks in their annual reports, there is no formal requirement for cyber risk disclosures.

Providing more proportionate disclosures that reflect the level of cyber risk will increase the confidence about insurers’ resilience and will ease the transition to new regulation in case cyber disclosures become mandatory following other countries’ examples.

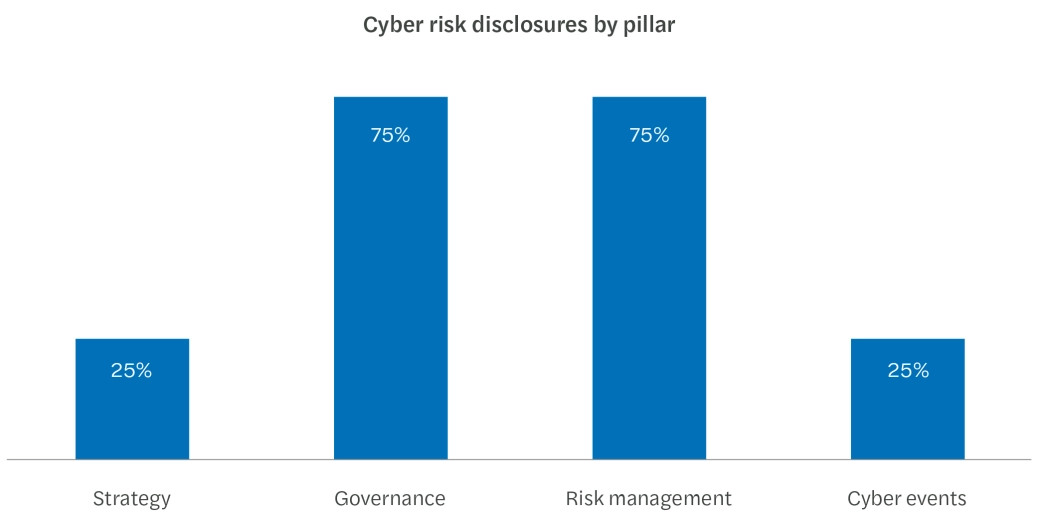

The FRC’s lab Digital Security Risk Disclosure report highlights good practices in cyber risk disclosures under four pillars: strategy, governance, cyber risk management, and cyber incident reporting. Whilst all the annual reports of UK LSE-listed insurers confirm the importance of cyber risk throughout their annual reports, the level of details provided varies significantly when assessing across these four pillars. The chart below shows that while many listed insurers provide details on cyber risk management and governance, the majority lack detailed disclosures on cyber risk strategy.

This analysis demonstrates that to provide more useful information about cyber risk and give sufficient confidence to the users of the annual reports, the majority of insurers will need to explain their cyber risk strategy better. In their annual reports, insurers should explain how their cyber risk strategy is customised to their unique risk profile, which includes their IT systems, data, and processes. Some examples of what aspects insurers could consider when disclosing cyber risk strategy include:

The escalating cyber risk landscape demands that insurers adopt more comprehensive and proportional disclosure practices. By aligning cyber risk reporting with the actual level of threat, insurers can enhance transparency and build confidence among stakeholders. Effective cyber risk disclosures should be tailored to each insurer's unique risk profile, integrating strategies for underwriting, third-party services, sales channels, AI automation, and risk reporting. Balancing detail with security considerations is crucial to avoid over-disclosure that could inadvertently increase vulnerability. As cyber threats continue to evolve, insurers must remain vigilant and proactive in their risk management and reporting practices, ensuring they are well-prepared to navigate the complexities of the digital age.

To speak to our experts about cyber risk disclosures, get in touch using the form below.

[1] IBM Report: Escalating Data Breach Disruption Pushes Costs to New Highs

[2] GB Cyber Insurance Market Update H1 2023 - WTW

[3] Cyber Realistic Disaster Scenario Development and Modelling

Select your interests and receive our latest insights, event invitations, news and more.

Read our latest insurance insights.

Having accessible technical accounting expertise/support is becoming increasingly important for corporate reporting purposes. Regulators are placing growing demands on businesses to report more transparently and on wider topical issues. Our approach is to be proactive and flexible to provide you with the technical expertise as and when your business needs it.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.