Sign up to hear more from us

Select your interests and receive our latest insights, event invitations, news and more.

The business models of some UK insurers result in elevated exposure to liquidity risk. Despite this, management of liquidity risk does not receive as much attention or investment as capital and other risks.

The COVID-19 pandemic, 2022 “LDI Crisis” and the PRA’s Business Plan 24/25 remind firms of the importance of sound liquidity risk management. Insurers need to ensure they have the understanding and tools to effectively manage their liquidity risk.

Liquidity risk has historically received limited attention from insurers. However, this is not a risk they are immune to, as recent developments like the increased investment in illiquid assets, interest rate volatility and insurance shocks (from natural catastrophes and pandemics) remind us. This can threaten insurers’ liquidity, with potentially severe consequences. Despite this, insurers continue to focus considerably more resources and attention on the management of capital and other risks. In 2019, the PRA published SS5/19 setting out requirements in relation to the management of liquidity risk.

Effective liquidity risk management requires an understanding of an insurer’s specific profile of liquidity sources/needs and the risks to which they are exposed. These exposures can be quite different from capital exposures, so a bottom-up analysis is important.

Insurers’ assets are generally quite liquid, while liabilities are fairly illiquid. Despite this, certain business models and recent developments can give rise to significant liquidity risk exposures:

Correlations exist between many of these risks and need to be evaluated and modelled. For example, a major natural catastrophe could impact asset values and an insurer’s rating.

Infrastructure for monitoring liquidity risk is often an afterthought, built off existing reporting systems with limited investment.

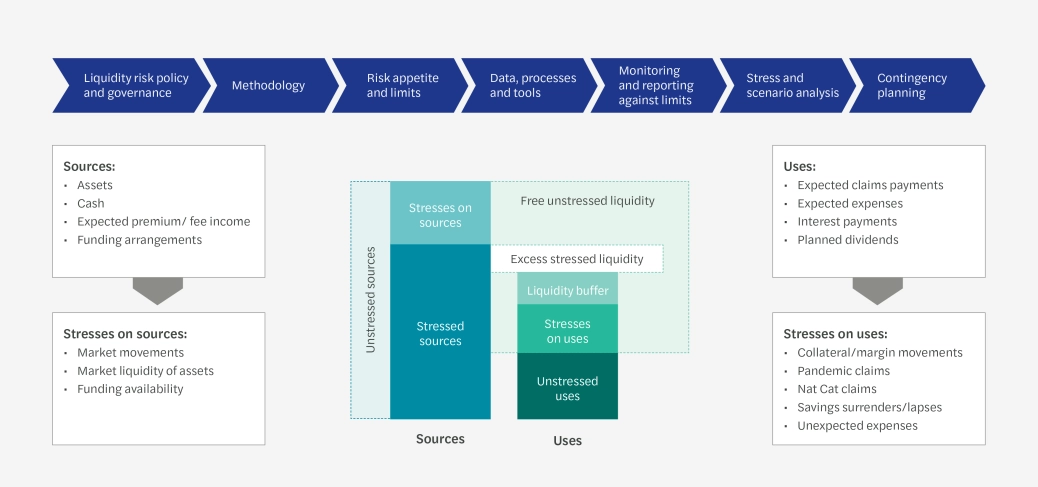

There are many factors insurers need to consider in designing a liquidity risk management framework. The framework should be set out in a liquidity risk policy covering responsibilities, appetite and governance.

The framework should clearly state a methodology that considers all material sources and uses of liquidity, and the risks they are each exposed to. The risks should be stressed with the methodology specifying the stresses, their severity and time horizons over which liquidity is measured. Several time horizons may be needed depending on the firm’s liquidity volatility.

Appropriate metrics are needed to measure liquidity risk and can be used to set risk appetite and limits. The Liquidity Coverage Ratio (LCR) is commonly used but excess stressed liquidity may be more meaningful and can also reflect risk appetite by applying a multiple to the stressed uses.

1 Multiple reflects risk appetite/limit

Regular monitoring and reporting of liquidity is needed. This may be needed frequently, e.g. if the firm’s liquidity is highly exposed to market movements or in times of heightened liquidity stresses. Accurately projecting future cash flows with the time granularity required for liquidity management may require adjustments to traditional actuarial data, processes and tools. Liquidity analysis needs to be performed at a level that reflects legal constraints on the transfer of liquidity, e.g. legal entity or fund level, consolidation has little meaning in this context without unrestricted fungibility.

Stress and scenario testing is a useful tool to understand liquidity risk exposures to financial market movements and sudden insurance losses. It can also inform contingency planning. Material transactions should be assessed for their impact on liquidity metrics. Additionally, key liquidity metrics should be included in the ORSA process and report.

Governance around actions to take in the event of insufficient liquidity should be clearly set out. A liquidity contingency plan should outline the potential options to improve liquidity and the priorities/situations under which the actions will be taken.

Liquidity shocks can pose a major risk to insurers. Firms must invest time and resources to ensure they understand the liquidity risks arising from their business models and have sufficient tools and capabilities to effectively manage these risks.

Speak with our financial services experts about liquidity risk management

|

Select your interests and receive our latest insights, event invitations, news and more.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.