Infrastructure insights

Read our latest infrastructure insights.

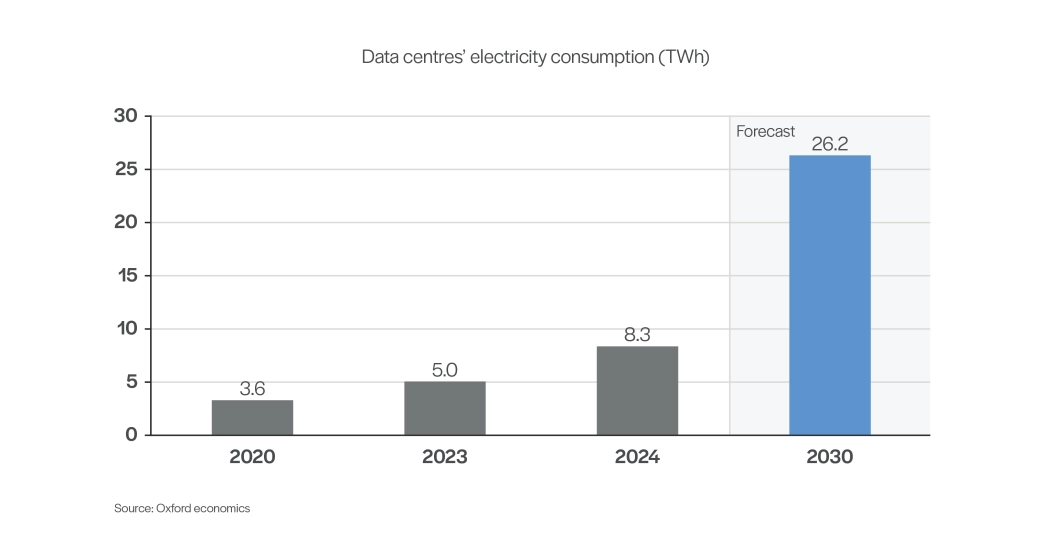

Demand has increased rapidly over the past five years, driven by the growth of artificial intelligence and high-performance computing, the continued expansion of cloud and hyperscale platforms, and the increasing requirements around data security and digital sovereignty. This growth is reflected in power consumption, with the UK data centre electricity demand reaching approximately 8.3 TWh in 2024, a significant increase from 3.6 TWh in 2020 [1].

Our experts are actively working with data centre clients across the UK, supporting them across a range of areas including financial model audit, assurance and due diligence. This article is the first in a series that will explore the market from the perspective of our clients, focusing on the key themes shaping the sector. Here, we set out the fundamental drivers of growth and outline some of the initial challenges developers are currently facing.

Demand for data centre capacity in the UK is being driven by a combination of structural and technology-led factors.

Artificial intelligence and cloud adoption are increasing demand for data centre capacity in the UK. AI usage across UK businesses has risen from approximately 9% in 2023 to around 23% in 2025, increasing the need for high-density computer infrastructure. Cloud adoption is already widespread, with around 69% of UK firms using cloud-based systems, and it underpins most AI deployment [2]. This is consistent with findings from our global C‑Suite Barometer for 2026, which shows that 44% of energy and infrastructure leaders believe AI will have the biggest impact on the success of their transformation, highlighting strong executive‑level demand for AI‑enabled infrastructure.

There is also a growing focus on data security and digital sovereignty. Organisations are placing greater importance on where data is stored and processed, particularly for sensitive or regulated workloads. This is contributing to demand for domestic data centre capacity within the UK. In parallel, the UK Government has formally recognised the strategic importance of the sector by designating data centres as Critical National Infrastructure in 2024, placing them alongside sectors such as energy and water [3]. This classification reflects the role data centres play in supporting essential services and the wider economy and reinforces their importance within national infrastructure planning.

The UK data centre market includes a range of facility types, which differ by function, customer base and scale. These distinctions are important when assessing demand, development requirements and investment activity. Facilities range from:

The market can also be understood by operator type. It includes hyperscale operators such as Amazon Web Services, Microsoft Azure and Google Cloud, alongside colocation providers such as Equinix and Digital Realty. These different models have distinct requirements in terms of scale, power and location. However, new development is increasingly driven by hyperscale data centres, which accounted for over 60% of construction activity in 2025 and are expanding to support cloud and AI workloads. Edge data centres remain a smaller segment, representing approximately 15% of development activity, typically focused on low-latency applications [4].

Geographically, the market is concentrated in London and the Southeast, which account for more than 80% of the UK capacity. Other clusters include Newport/Cardiff and Manchester, although these remain smaller in scale. There are estimated to be over 500 data centres across the UK, depending on classification [5].

This concentration is beginning to shift as developers look for locations with better access to power and more flexible planning environments. Scotland is increasingly being considered as a potential growth market, supported by access to renewable energy, land availability and policy support for digital infrastructure. In 2025, Scotland attracted about 8% of investment in UK Data Centre construction, which is proportionate to the size of Scotland's GDP. We will explore the specific factors contributing to Scotland’s attractiveness in the next article of this series.

The value of data centre assets is closely linked to how effectively these challenges are managed. Access to power, planning certainty and location strategy are key factors in determining the attractiveness and performance of an asset.

In future articles in this series, we will uncover details on data centre valuation, transaction dynamics, financial model construction and the factors that distinguish high‑quality assets in this rapidly evolving sector.

Get in touch with our Energy and Infrastructure experts

|

[1] The UK’s data centre boom: growth trends, drivers, and the rising power challenge | Oxford Economics

[3] Written statements - Written questions, answers and statements - UK Parliament

[4] United Kingdom Data Center Construction Market Size, Share & Trends Report 2025 - 2031

[5] UK Data Centres Outlook 2026 | CBRE UK

[6] NESO reveals results of UK's grid connection reforms - DCD

Read our latest infrastructure insights.

Discover how to boost business success and resilience through technology and strengthen its protection, compliance and security.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.