IASB publishes an exposure draft on accounting for dynamic interest rate risk management activities

11 March 2026

Tags

Financial services

Insights

Upcoming IFRS Amendments – Proposals to account for dynamic interest rate risk management activities.

What is the issue?

The exposure draft Risk Mitigation Accounting – Proposed Amendments to IFRS 9 and IFRS 7, published by the IASB in early December 2025, sets out a proposed new accounting approach intended to reflect dynamic interest rate risk management activities in financial statements.

Given the complexity of this new accounting model, the IASB has established an exceptional 240‑day comment period, ending on 31 July 2026. In addition to written comments, the IASB is inviting preparers to participate in fieldwork designed to test how the model operates in practice based on their own specific circumstances.

This article aims to summarise:

- the context and objectives of the proposed amendments;

- the structure and components of the new accounting approach developed by the IASB;

- the methods used to recognise and measure dynamic interest rate risk management activities;

- the principles that apply when the model is discontinued;

- the proposed transition requirements for first‑time application; and

- the new disclosure obligations introduced by the proposals.

Background and objectives

What is dynamic risk management?

Dynamic risk management is a practice most commonly observed in financial institutions.

Because their core activities, such as granting loans, collecting deposits and issuing long‑term insurance contracts, expose them to uncertainty about future earnings, these institutions face significant unpredictability arising from fluctuations in interest rates. This exposure is referred to as interest rate risk.

For banking institutions, for example, this risk stems from a combination of factors:

- A rate mismatch on the balance sheet: differences in the rate characteristics of assets and liabilities (fixed versus variable) create uncertainty about the bank’s future net interest margin. For instance, if all assets are fixed‑rate while all liabilities are variable‑rate, the bank becomes exposed to a decline in its net interest margin if interest rates rise.

- A mismatch in nominal amounts and maturities: future liquidity needs or surpluses require refinancing or reinvestment transactions, which, when combined with rate mismatches, may introduce uncertainty about future net interest margins. For example, if all transactions are fixed‑rate, and all assets mature in ten years while liabilities fall due in one year, the bank becomes exposed to a deterioration in its net interest margin if interest rates rise during the first year, as the refinancing required in one year’s time will occur at a higher rate.

- The objective of dynamic risk management (also referred to as asset and liability management) is therefore to:

- quantify the interest rate risk arising from all current and expected future transactions (including assets, liabilities and, where relevant, forecast transactions); and

- reduce this risk to a level consistent with the institution’s risk appetite, typically through the use of interest rate derivatives.

Why a new model?

Since the initial application of IFRS 9 Financial Instruments, the transitional provisions have allowed entities, for hedge accounting purposes, either to apply the hedge accounting requirements of IFRS 9 or to continue applying those of IAS 39. Many financial institutions have chosen to retain IAS 39 in order to document interest rate hedging derivatives within portfolio hedging relationships.

This transitional relief was intended to give the IASB sufficient time to develop a new accounting model for macro‑hedging relationships before IAS 39 is ultimately withdrawn.

The need for a new model arises because the existing hedge accounting requirements (in both IFRS 9 and IAS 39) only permit hedge documentation based on closed and stable portfolios of hedged items. These requirements do not adequately portray dynamic risk management strategies, in which an entity manages interest rate risk on a net basis across open portfolios that evolve continuously as a result of new business, repayments and repricing events.

The exposure draft therefore proposes a new accounting framework - Risk Mitigation Accounting (RMA) - designed to better reflect the economic effects of dynamic interest rate risk management strategies in financial statements. Without such a model, the removal of IAS 39 would lead to an accounting mismatch between the measurement of derivatives used for risk mitigation and the measurement of the underlying portfolios that give rise to repricing risk.

Repricing risk refers to the risk that the benchmark interest rates applicable to financial assets and liabilities will reprice at different times, for different amounts or based on different benchmark curves. This risk primarily affects financial institutions such as banks and insurers, which typically manage interest rate risk with a dual objective: reducing both the variability of future cash flows and the variability of the fair value of the underlying portfolios.

What does this mean?

Scope of application

The proposed model is intended for entities whose activities give rise to financial instruments exposed to interest rate repricing risk and that mitigate this risk on a net basis using interest rate derivatives.

It is applied at the level at which the entity manages repricing risk on a net basis, for example, by currency, by legal entity or by the benchmark interest rate to which the instruments are linked.

Application of the model is optional, and it may only be used if the entity formally documents its risk management strategy and the conditions under which the RMA model is applied. However, if an entity that falls within the scope of the RMA chooses not to apply the model, it must still provide disclosures in the notes describing its exposure, its risk management processes and how its risk management activities are reflected in its financial statements.

Structure and components of the proposed model

Compared with the current hedge accounting requirements, the RMA introduces new concepts that underpin the accounting treatment of dynamic interest rate risk management activities. To accommodate these concepts, the exposure draft proposes adding a new section to IFRS 9, positioned after the existing hedge accounting guidance.

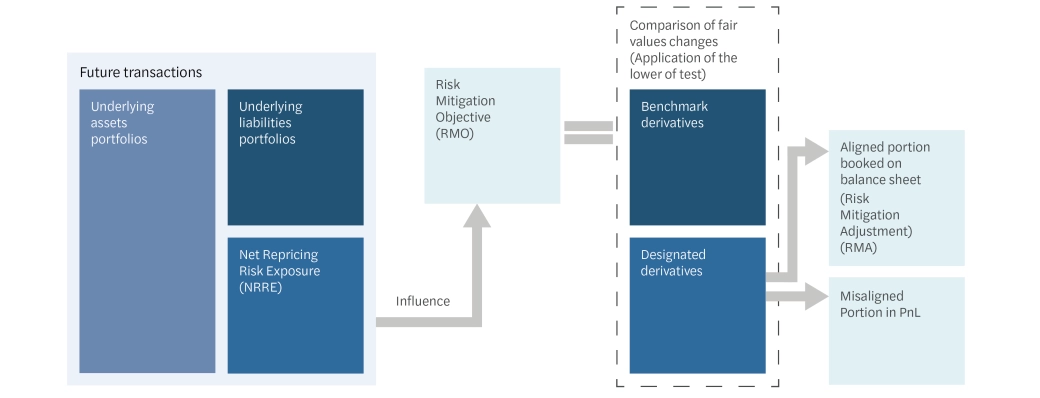

Underlying portfolios

The following items qualify as underlying portfolios:

- financial assets measured at amortised cost or at fair value through other comprehensive income;

- financial liabilities measured at amortised cost; and

- future transactions, which may include firm commitments, expected reinvestments or refinancing of existing operations, and highly probable forecast transactions.

Financial instruments measured at fair value through profit or loss and equity instruments are excluded, as they do not create the type of accounting mismatch that the RMA model is intended to resolve.

In addition, the stable portion of demand deposits may be treated as fixed‑rate liabilities when they are exposed to repricing risk on a portfolio basis.

Net repricing risk exposure

The entity aggregates the repricing risk arising from the underlying portfolios into future maturity bands, based on the expected repricing dates. These dates are determined using factors such as contractual terms and behavioural assumptions. The metric selected to quantify exposure must be consistent with the entity’s internal risk management practices, such as the nominal gap or the sensitivity of the economic value of equity.

Designated derivatives

Only interest rate derivatives entered into with external counterparties, such as swaps, forward rate agreements, futures and options, are eligible for designation. Net written options and derivatives whose fair value changes are driven predominantly by risks other than interest rate risk are excluded, except where a written option profile offsets a purchased option position.

Risk mitigation objective

The risk mitigation objective represents the absolute amount of net repricing risk to be mitigated within each maturity band. It is influenced by the position of designated derivatives and cannot exceed the net organic exposure, meaning the exposure before considering the effects of designated derivatives. The objective must be expressed using the same measurement basis that management applies internally and must be updated whenever the entity undertakes new risk management actions, such as entering into interest rate derivatives to hedge its net exposure.

Benchmark derivatives

To measure the risk mitigation objective and monitor it over time, the entity constructs theoretical benchmark derivatives (similar in concept to the hypothetical derivative used in cash flow hedge accounting) which replicate the timing and amount of the mitigated risk independently of the designated derivatives. These benchmark derivatives are designed to have an initial fair value of zero.

If unexpected changes occur in the net exposure, for example, if early repayments exceed expectations, the entity adjusts the benchmark derivatives to reflect the portion of exposure that no longer exists relative to the new net exposure.

Recognising and measuring the risk mitigation adjustment

An alternative accounting policy to hedge accounting

The accounting approach proposed by the IASB in the exposure draft is neither fair value hedge accounting nor cash flow hedge accounting.

Under this new model, designated derivatives are measured at fair value, with the resulting changes allocated as follows:

- recognition, on a separate line in the statement of financial position, of a risk mitigation adjustment representing the portion of the derivative’s fair value that effectively mitigates variability arising from repricing risk; and

- immediate recognition in profit or loss of any remaining portion, in a manner similar to the treatment of ineffectiveness in a cash flow hedge.

Recognising the risk mitigation adjustment in the statement of financial position

The risk mitigation adjustment is measured as the lower of the cumulative gains or losses on the designated derivatives and the cumulative change in the fair value (present value) of the benchmark derivatives.

Accordingly, if the cumulative gains or losses on the designated derivatives exceed the cumulative change in the fair value of the benchmark derivatives, the excess is recognised immediately in profit or loss. This excess reflects differences between the characteristics of the designated derivatives and those of the benchmark derivatives, which may be structural (for example, differences in benchmark interest rates or maturities) or may arise from unexpected changes in net exposure that required adjustments to the benchmark derivatives (such as changes in maturity or notional amounts).

The IASB acknowledges that the risk mitigation adjustment does not meet the strict definition of an asset or a liability in the Conceptual Framework. However, it considers this departure necessary to provide useful information, as it avoids the volatility that would result from recognising gains and losses on designated derivatives in other comprehensive income.

The following diagram summarises the structure of the model and the recognition principles:

Recognising the risk mitigation adjustment in profit or loss

The cumulative risk mitigation adjustment on the statement of financial position is recognised in profit or loss during the same reporting period as the repricing differences arising from the underlying portfolios in order to mitigate their effect.

RMA excess test

At each reporting date, the entity must assess whether there is any indication that the risk mitigation adjustment may not be fully realised over the mitigated time horizon. This situation may arise when unexpected changes in net repricing risk exposure during the reporting period have not been fully captured through adjustments to the benchmark derivatives.

If such an indication exists, the entity must determine whether the accumulated risk mitigation adjustment exceeds the present value of the net repricing risk exposure at the reporting date.

If an excess amount is identified in absolute terms, that amount must be recognised immediately in profit or loss, with no possibility of subsequent reversal.

Discontinuation and transition requirements

Discontinuation of risk mitigation accounting

An entity is required to discontinue the use of the RMA approach prospectively when there is a change in its risk management strategy, for example, a change in the benchmark rate being mitigated, the scope of risk management activities or the measurement indicator used to quantify exposure. However, an entity may not discontinue risk mitigation accounting solely by choice.

When discontinuation does occur, the entity must recognise in profit or loss the amount accumulated as the risk mitigation adjustment:

- over time, when repricing differences arising from the underlying portfolios are still expected to affect future results; or

- immediately, when repricing differences from the underlying portfolios are no longer expected to affect profit or loss.

Transition requirements

The exposure draft proposes that the new RMA model may only be applied prospectively. Accordingly, on the date of first application:

- entities that have documented macro‑hedging relationships under IFRS 9 or IAS 39 may discontinue those hedging relationships in order to apply the RMA approach, with remeasurement differences recognised under the previous model permitted to be amortised over the remaining hedging period;

- entities that have designated financial assets or liabilities at fair value through profit or loss may revoke that designation so that the items can be included in the underlying portfolios of the RMA model, using their fair value on the transition date as their amortised cost.

Presentation and disclosures (amendments to IFRS 7 and IFRS 18)

Presentation in the primary financial statements

In the statement of financial position, the risk mitigation adjustment must be presented on a separate line, classified as either an asset or a liability depending on the direction of the cumulative gains and losses on the designated derivatives.

In the statement of profit or loss, the recognition of gains and losses arising from the risk mitigation adjustment must also be presented on a separate line.

Disclosures (amendments to IFRS 7)

New disclosures must be provided in a dedicated note, focusing on:

- the entity’s repricing risk management strategy (including the level at which it is applied, its frequency, timing and processes);

- the effect of designated derivatives on the amount, timing and uncertainty of future cash flows (including schedules of designated derivatives, average fixed rates and sensitivity analyses); and

- the effect of risk mitigation accounting on the statement of financial position and on profit or loss (including qualitative and quantitative information on underlying portfolios, designated derivatives, the RMA measurement methodology and the expected profile of RMA recycling to profit or loss).

Classification of gains and losses on derivatives (amendments to IFRS 18)

These amendments aim to incorporate designated derivatives under the RMA model into the requirements governing the classification of gains and losses on derivatives in the statement of profit or loss. As a result, gains and losses will be classified in the same category as the income and expenses affected by the managed risk, while avoiding any grossing‑up of amounts.

Conclusion

This exposure draft, which introduces a new accounting model for macro‑hedging, is the culmination of extensive work initiated in 2018.

The IASB aims to:

- more faithfully reflect how financial institutions manage interest rate risk by permitting the hedging of an aggregate net position comprising open portfolios of assets and liabilities, including demand deposits;

- better portray the accounting effects of this risk management by affecting profit or loss only when over‑hedging occurs or when an excess is identified in the risk mitigation adjustment; and

- establish an approach that is operational for preparers and that limits volatility in equity, and therefore in prudential own funds, through the innovative RMA mechanism, even though it represents a departure from the IASB’s Conceptual Framework.

When is it effective?

The IASB has set an extended comment period to the end of July 2026 due to the complexity of the proposals. Stakeholders are encouraged to participate in fieldwork to test the model’s operability before the IASB finalises the standard. The effective date will be determined after redeliberations.

Who is it applicable to?

The proposals primarily apply to financial institutions, such as banks and insurers, that manage interest rate repricing risk dynamically on a net basis and use interest rate derivatives for risk mitigation. Entities adopting RMA must comply with the full recognition, measurement, presentation and disclosure requirements. Entities that qualify but choose not to apply RMA must still provide enhanced disclosures on their exposure and risk management processes.

Key contact

Technical issues trending now – H1 2026

Technical insights, UK GAAP and IFRS publications.