In the third instalment of our ‘What’s next in Insurance reporting five priorities for 2027 and beyond’ series, we focus on AI and how with the adoption rate the sector is experiencing, its relevance in corporate reporting and financial statements cannot be underestimated.

AI is reshaping insurers’ core operations

According to the Artificial Intelligence in UK Financial Services survey conducted by the Bank of England and the Financial Conduct Authority in 2024 [1], the insurance sector reported the highest adoption of AI, with 95% of firms currently using the technology. Within the financial services industry, general insurance represents the third largest area of AI deployment, followed by operations and IT, and retail banking.

For the insurance industry, AI offers a range of benefits across core business activities. These include more efficient claims automation and assessment, enhanced underwriting and pricing accuracy, improved fraud detection and financial crime prevention, more responsive customer support, and improved regulatory horizon scanning. An insurer’s ability to understand, govern and implement AI appropriately therefore has the potential to reshape business processes, improve efficiency and support strategic decision-making.

However, the adoption of AI also introduces new and significant risks. These include increased exposure to cyber-attacks, more sophisticated fraudulent activity, reliance on complex and opaque models, and greater sensitivity to data quality and governance weaknesses.

AI is outpacing traditional governance frameworks

The evolution of AI has notably accelerated in recent years. While concepts such as machine learning and deep learning have existed for decades, the emergence of generative AI and, since 2022, more autonomous systems has significantly expanded both the accessibility and scope of AI applications.

The FCA and PRA are currently taking a principle-based, technology-neutral approach to AI in financial services. They expect firms to manage AI risks within existing regulatory frameworks while enabling responsible innovation rather than introducing prescriptive AI specific rules. There is however ongoing work in this area, such as the FCA’s long term review into AI (‘the Mills Review’).

Capabilities are evolving faster than governance frameworks, regulatory guidance and established best practice. As a result, AI tools are increasingly being deployed in areas with a more direct influence on financial outcomes and reported results than earlier generations of technology.

Insurers view AI as an existing risk rather than a purely strategic opportunity

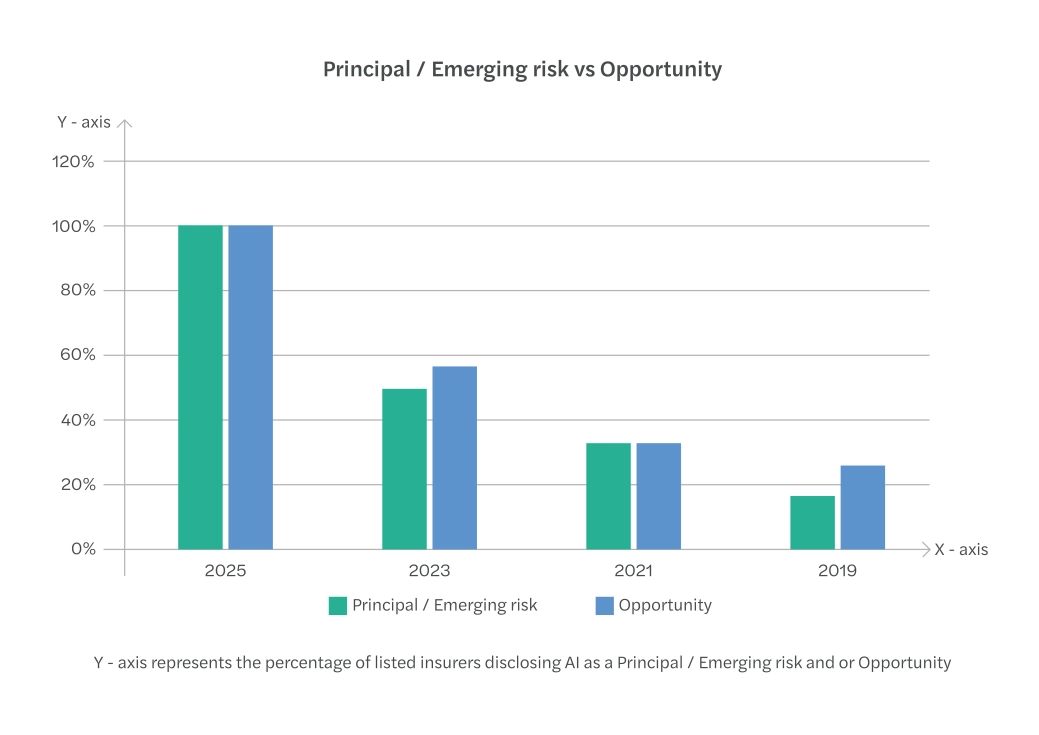

Our analysis of twelve London Stock Exchange (‘LSE’) listed insurers’ annual reports (see Figure 1), covering both life and non-life companies, illustrates how attitudes toward AI have evolved over time. Emerging risks and opportunities are typically discussed in the front sections of annual reports, where principal risks and uncertainties are disclosed.

The chart highlights that all listed insurers now reference artificial intelligence in their annual reports, signalling its growing prominence across the sector. As of 2025, insurers consistently frame AI as both an opportunity and a risk. Firms are becoming more receptive to AI’s potential as an efficiency‑enhancing tool, while remaining alert to its capacity to intensify existing risk exposures, including cyber risk, operational resilience challenges, data governance concerns, and model risk.

AI is becoming relevant to corporate reporting

At present, there are no specific reporting requirements relating to AI, nor explicit disclosure standards addressing AI-related risks. However, the pace of technological change and the evolving tone of insurers’ disclosures indicate that AI is becoming an increasingly relevant consideration for users of financial statements.

There is therefore a case for insurers to consider whether existing disclosures adequately reflect their exposure to AI-related risks and the governance frameworks in place to manage them. In particular, what insurers may wish to consider in relation to AI is:

- Governance: oversight structures, policies and responsibilities for the use of AI.

- Risk identification: clear articulation of AI-related risks, including interactions with cyber risk, model risk and operational resilience.

- Risk management: how AI risks are monitored, controlled and responded to.

- Impact on financial reporting: where relevant, how AI influences key judgements, estimates or reporting processes.

This approach mirrors the development of climate risk disclosures and was leveraged by FRC for digital security risk reporting recommendations in the FRC Lab report[2].

AI-related disclosures are an indicator of resilience and control

AI is already influencing how insurers operate and make decisions, and its role is likely to grow. While the full financial implications remain uncertain, insurers increasingly recognise AI as an existing risk rather than a purely strategic opportunity.

Unlike some longer-term emerging risks, AI has the potential to give rise to more immediate consequences if not appropriately governed. In this context, corporate reporting has an important role to play. Clear, balanced disclosures can help users understand how insurers are governing AI, managing associated risks and safeguarding the reliability of reported information. As expectations evolve, the quality of AI-related disclosures may become an important indicator of an insurer’s overall resilience and control environment.

Get in touch with our insurance experts

To discuss how AI might impact your organisation, speak with one of our experts via the contact button below.

Contact us today

References

[1] Artificial intelligence in UK financial services - 2024 | Bank of England

[2] FRC Digital Security Risk Disclosure Example Bank_August 2022